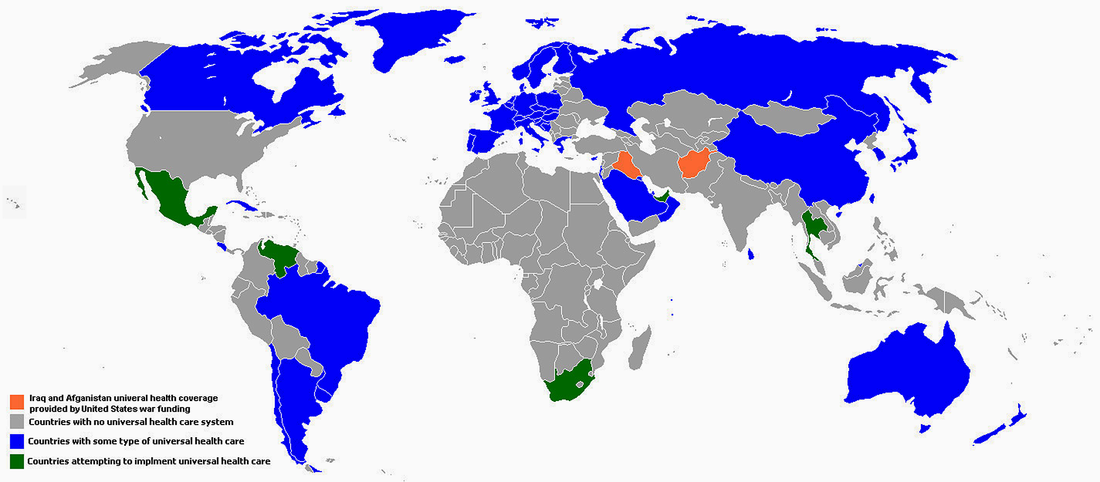

Whenever I ponder the prospect of national Universal Healthcare being enacted in this country, I can’t help but think of the 58 nations around the world who are operating various “working models” of it – and then I can’t also help but think their shared response in possibly NOT having it is one that is an obvious “affront to humanity” and the “basic rights of human beings not to needlessly suffer and die.” For some it may be a “divine calling” or just something that comes from their own sense of “spirituality,” but all I have ever seen of America’s exclusionary and profit-driven “Have or Have-Not Healthcare Marketplace Patchwork” is that it is the most exploitive and punitive “affronts to American humanity.”

In actuality, getting to Universal Healthcare is a lot EASIER than most people would think in a country which is seemingly mired in the collective mindset, “America is way different than the rest of the world and far more complex given its size to mount a Herculean endeavor of this scale.”

That could be furthest thing from the truth…and that’s what the “Special Interest” forces originating out of Big Healthcare, Big Health Insurance and Big Pharma working their century-long propaganda spinning in the halls of power in Washington, D.C., have been consistently weaving into the American public narrative about Universal Healthcare. We’ve heard all of the cries: “Socialized medicine is Communism, it’s the rise of the Nanny Socialist State, it’s Big Government which will bankrupt this country!”

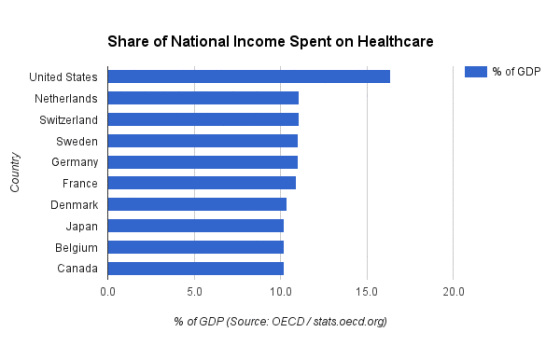

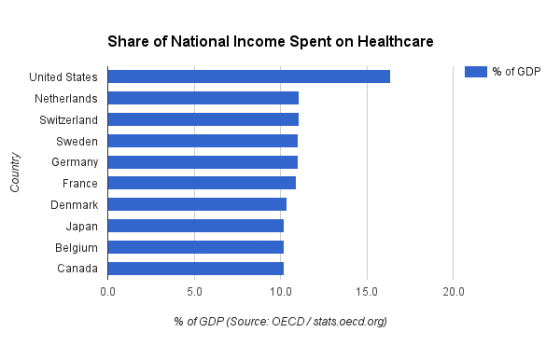

What’s lost in all this is that in all of the other 58 countries operating various forms of Universal Healthcare systems is that they all substantially bring down medical and coverage costs. It not only translates to SUBSTANTIAL savings for their citizens and businesses but also has “spillover benefits” by increasing workplace productivity, reducing mortality rates, relieving consumers from ever having to file bankruptcies (because of prohibitive “out-of-pocket” medical costs, and the general physical and mental well-being of their citizenry). And as the bar chart below and from Part III in this blog attest, the closest of the OECD developed nations is 50-percent or more lower in the healthcare expenditures as a percentage of their Gross Domestic Product (GDP) than the world’s perennial cost leader, the United States of America (17.5-percent of its GDP or $3.3 TRILLION goes to healthcare spending).

In actuality, getting to Universal Healthcare is a lot EASIER than most people would think in a country which is seemingly mired in the collective mindset, “America is way different than the rest of the world and far more complex given its size to mount a Herculean endeavor of this scale.”

That could be furthest thing from the truth…and that’s what the “Special Interest” forces originating out of Big Healthcare, Big Health Insurance and Big Pharma working their century-long propaganda spinning in the halls of power in Washington, D.C., have been consistently weaving into the American public narrative about Universal Healthcare. We’ve heard all of the cries: “Socialized medicine is Communism, it’s the rise of the Nanny Socialist State, it’s Big Government which will bankrupt this country!”

What’s lost in all this is that in all of the other 58 countries operating various forms of Universal Healthcare systems is that they all substantially bring down medical and coverage costs. It not only translates to SUBSTANTIAL savings for their citizens and businesses but also has “spillover benefits” by increasing workplace productivity, reducing mortality rates, relieving consumers from ever having to file bankruptcies (because of prohibitive “out-of-pocket” medical costs, and the general physical and mental well-being of their citizenry). And as the bar chart below and from Part III in this blog attest, the closest of the OECD developed nations is 50-percent or more lower in the healthcare expenditures as a percentage of their Gross Domestic Product (GDP) than the world’s perennial cost leader, the United States of America (17.5-percent of its GDP or $3.3 TRILLION goes to healthcare spending).

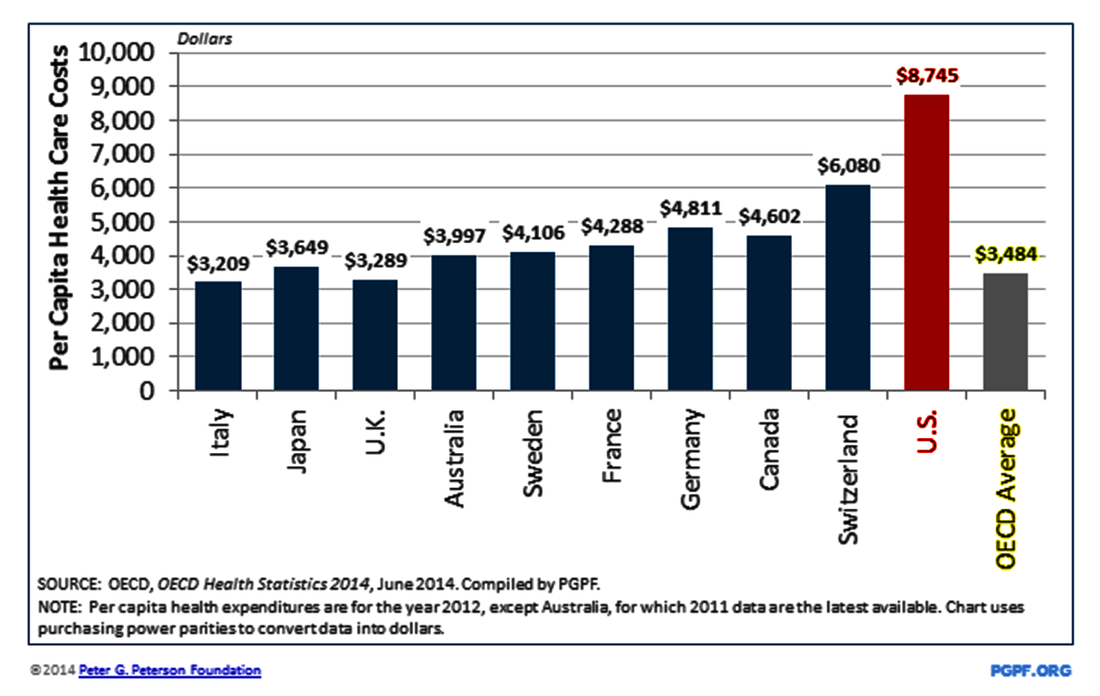

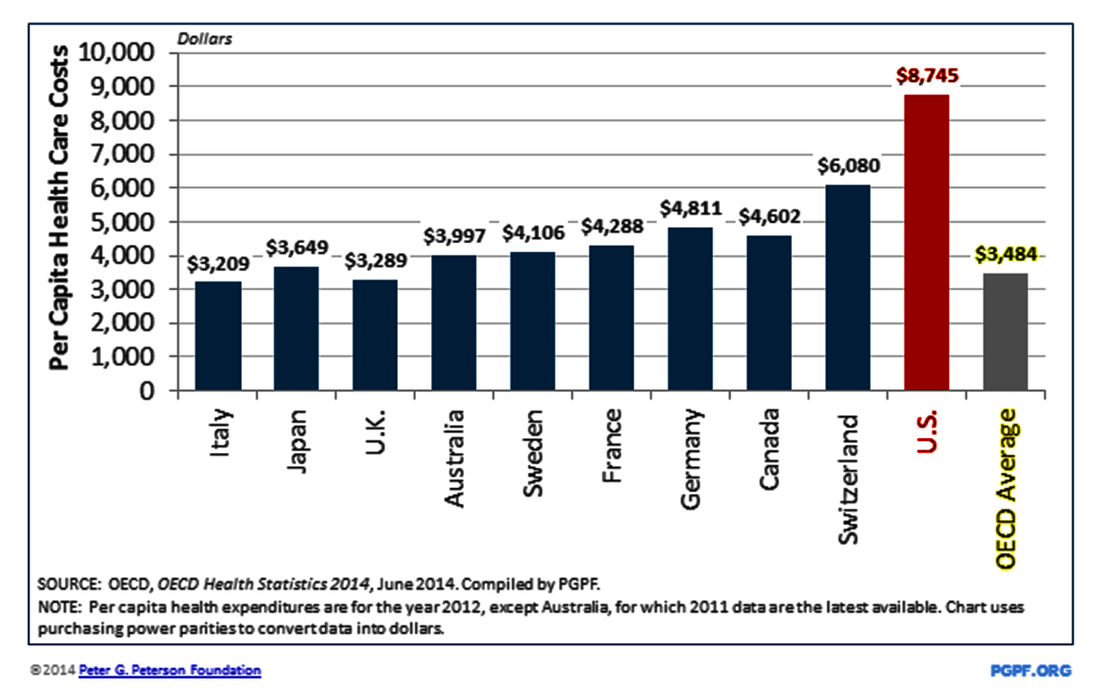

In fact the per-capita cost of healthcare in the United States is actually pushing over the $9,000-per-person barrier in 2016, according to more recent Kaiser Family Foundation and OECD estimates and projections. During the most recent complete per-capita analysis of the year 2012, OECD’s pegging America at an $8,745 per-capita healthcare cost in 2012, it represented a whopping 151%-percent over what the 10-nations of OECD average of $3,484 per-capita in health expenditures – with all 9 of the other OCED nations operating and offering Universal Healthcare systems of various forms.

Switzerland comes the closest to cost-leader USA, about 44%-percent lower with $6,080 in annual per-capita healthcare costs in 2012. Although Switzerland remains a nation offering Universal Healthcare, it is described more as “statutory health insurance,” possibly the closest to the U.S. in having its 26 cantons oversee a number of “licensed third-party insurance providers” which still have to nonetheless following “price control guidelines” in each of the cantons to feed federal statutes – about the closest a Universal Healthcare system comes to America’s largely “private marketplace economy” of “American Have or Have-Not Healthcare” since being left in place at the turn of the 19th to 20th century.

Switzerland comes the closest to cost-leader USA, about 44%-percent lower with $6,080 in annual per-capita healthcare costs in 2012. Although Switzerland remains a nation offering Universal Healthcare, it is described more as “statutory health insurance,” possibly the closest to the U.S. in having its 26 cantons oversee a number of “licensed third-party insurance providers” which still have to nonetheless following “price control guidelines” in each of the cantons to feed federal statutes – about the closest a Universal Healthcare system comes to America’s largely “private marketplace economy” of “American Have or Have-Not Healthcare” since being left in place at the turn of the 19th to 20th century.

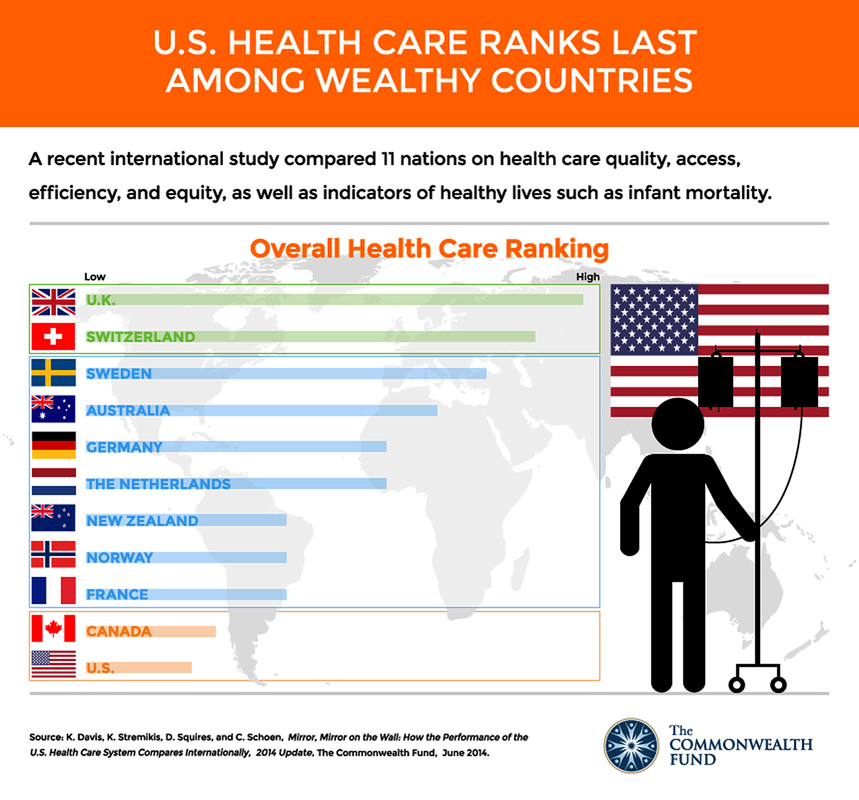

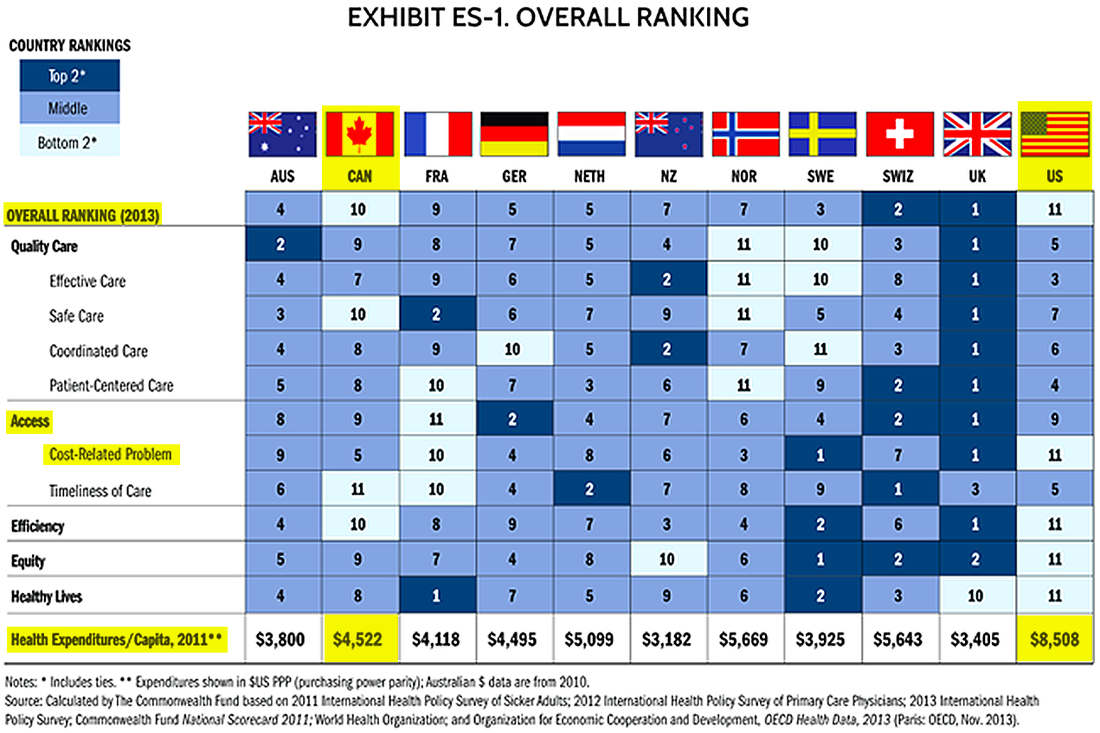

You would think with America’s annual “world cost leader” status that it would mean our citizenry has “access to the world’s best healthcare system,” but that would be the furthest from the truth in a number of key measures explored below. Among the 11 “wealthy nations” of the OECD in The Commowealth Fund bar chart below, there 10 “developed nations” – all featuring various forms of Universal Healthcare systems – that rank far above America in “Overall Health Care Ranking” based on such key measures as “access,” “health care quality,” “healthy lives” and “infant mortality” rates.

In the more specific tiered, color-coded rankings among the top 11 OECD nations in The Commonwealth Fund chart below, it should probably come as little surprise that the United States still holds the dubious last-place ranking (11th) in 2013. Outside of its still disappointing cellar-dweller status, what stands out is similar “Bottom 2”-tier last-place rankings when it comes to “cost-related problems” gaining health care “access” while the mish-mash of America’s so-called “open healthcare marketplace” patchwork sees our citizenry suffer with the “most-inefficient” to the “least healthy lives” outcomes of these major developed nations.

Over several years of The Commonwealth Fund research the United Kingdom’s universal healthcare-based National Health Service attained top rankings due to what researchers cited as increased investment and emphasis on direct (online) access to primary General Physicians (though some still see “gatekeeper access” to get health issue quickly addressed), Urgent Care Services. Hospitals, and Dentistry Care. However, in recent years, there have been some public outcry about the NHS and other public agency attempts to possibly close, sell or privatize certain government-owned hospitals, where bed occupancy rates and treatment costs were higher to maintain, particularly in lower-population rural areas of England.

No doubt, every healthcare system in the world has its system hiccups and “rationing” of healthcare services, but the glaring, growing inconsistencies of America’s Have or Have-Not Marketplace Patchwork of those two areas standout the most. If we can next take a look across from northern border into Canada, its “bottom-tier” 10th-ranking among the 11 OECD “wealthy” nations (just ahead of America) comes about as the provinces and territories created regional health authorities under the country’s similarly-titled Medicare single-payer universal healthcare national umbrella coverage in 1966 – ironically, the same year the U.S. federal government enacted its own version of national Medicare health coverage for the Seniors over-65 population in America.

The Canadian version of Medicare has had it share of issues in the 50 years since socialized Universal Healthcare has become a fixture across its 10 provinces and 3 territories of the British Commonwealth nation -- most notably with bottom rankings in Timeliness of Care (11th), Safe Care (10th) and Efficiency (10th) in The Commonwealth Fund ranking report.

The Canadian version of Medicare has had it share of issues in the 50 years since socialized Universal Healthcare has become a fixture across its 10 provinces and 3 territories of the British Commonwealth nation -- most notably with bottom rankings in Timeliness of Care (11th), Safe Care (10th) and Efficiency (10th) in The Commonwealth Fund ranking report.

With about 70-percent of Canada’s Medicare covered with “public funding” shared equally among the federal government in Ottawa and the other half by the provinces, there had been increase movement to “Private Insurance,” which covers services excluded from public reimbursement such as vision and dental care, prescription drugs, rehabilitation services, home care, and private rooms in hospitals. Still, at a $4,522 per-capita national expenditure (in U.S. dollar value), Canada’s healthcare costs are slightly less than HALF than what the United States spends.

When gauging the “popularity” of Universal Healthcare in Canada, an August 2009 poll conducted by Toronto-based Nanos Research pointed to overwhelming support – 86.2%-percent of 1,001 Canadians reached for response to random phone survey – called for “strengthening public health care rather than expanding for-profit services” in answer other outside special interests and political figures looking to “privatize” the provinces’ federated Medicare system.

Perhaps the most indelible statement from the Canadian public came in a 2004 CBC Television poll, when they voted for the late Tommy Douglas, the former premier of the Sasketchewan province who introduced and enacted the first “provincial form” of Universal Healthcare in 1948, to be honored as “The Greatest Canadian” in history for his vision being later eventually adopted across all 10 provinces, 3 territories and on the federal level by 1966.

To get perhaps the clearest yet broadest perspective on so-called “Socialized National Healthcare” practiced globally (if you have a little less than one hour’s time to invest by mouse-clicking the video below), PBS and Frontline’s 2009 “Sick Around the World” documentary provides the most definitive "globe-trotting" exploration of FIVE countries' -- England, Germany, Switzerland, Japan and Taiwan — differing "working models" of successfully applied Universal Healthcare systems. It provides a revealing exploration into the varying structural operational/funding architectures in each of these working models -- government-only, public/private, public/nonprofit, public/nonprofit/for-profit, etc. -- that can be easily deployed with an open-minded, spirit of "humane innovation" and basic government reforms and enactment.

When gauging the “popularity” of Universal Healthcare in Canada, an August 2009 poll conducted by Toronto-based Nanos Research pointed to overwhelming support – 86.2%-percent of 1,001 Canadians reached for response to random phone survey – called for “strengthening public health care rather than expanding for-profit services” in answer other outside special interests and political figures looking to “privatize” the provinces’ federated Medicare system.

Perhaps the most indelible statement from the Canadian public came in a 2004 CBC Television poll, when they voted for the late Tommy Douglas, the former premier of the Sasketchewan province who introduced and enacted the first “provincial form” of Universal Healthcare in 1948, to be honored as “The Greatest Canadian” in history for his vision being later eventually adopted across all 10 provinces, 3 territories and on the federal level by 1966.

To get perhaps the clearest yet broadest perspective on so-called “Socialized National Healthcare” practiced globally (if you have a little less than one hour’s time to invest by mouse-clicking the video below), PBS and Frontline’s 2009 “Sick Around the World” documentary provides the most definitive "globe-trotting" exploration of FIVE countries' -- England, Germany, Switzerland, Japan and Taiwan — differing "working models" of successfully applied Universal Healthcare systems. It provides a revealing exploration into the varying structural operational/funding architectures in each of these working models -- government-only, public/private, public/nonprofit, public/nonprofit/for-profit, etc. -- that can be easily deployed with an open-minded, spirit of "humane innovation" and basic government reforms and enactment.

Hosted and reported by Washington Post T.R. Reid. “Sick Around the World’s” whirlwind investigative exploration, Reid said his overall findings pointed to Three Common Tenets Of How Other World “Universal Healthcare” Systems Need To Operate Successfully (either as “Socialized/Public Care” or hybrid “Public/Private Universal Healthcare”):

- Insurance companies MUST COVER EVERYONE and CANNOT MAKE A PROFIT on “Basic Care Services” – they may charge a premium for certain “Supplemental Coverage” plans in certain countries. Most of the countries featuring some (if any) participation of “private health insurance providers” do not allow them to be attached to “public stock exchanges” and most governments can set limits on their pricing and profits;

- Everybody is (legally) “mandated” to buy insurance coverage and the governments pay for the POOR to have health coverage – many of the countries pay the “subsidized coverage” through higher taxes on the upper-middle class to the wealthy;

- Doctors and Hospitals have to accept “ONE SET STANDARD ON FIXED PRICING” for their services. Pricing levels are reviewed on either a quarterly or annual basis in some of these countries.

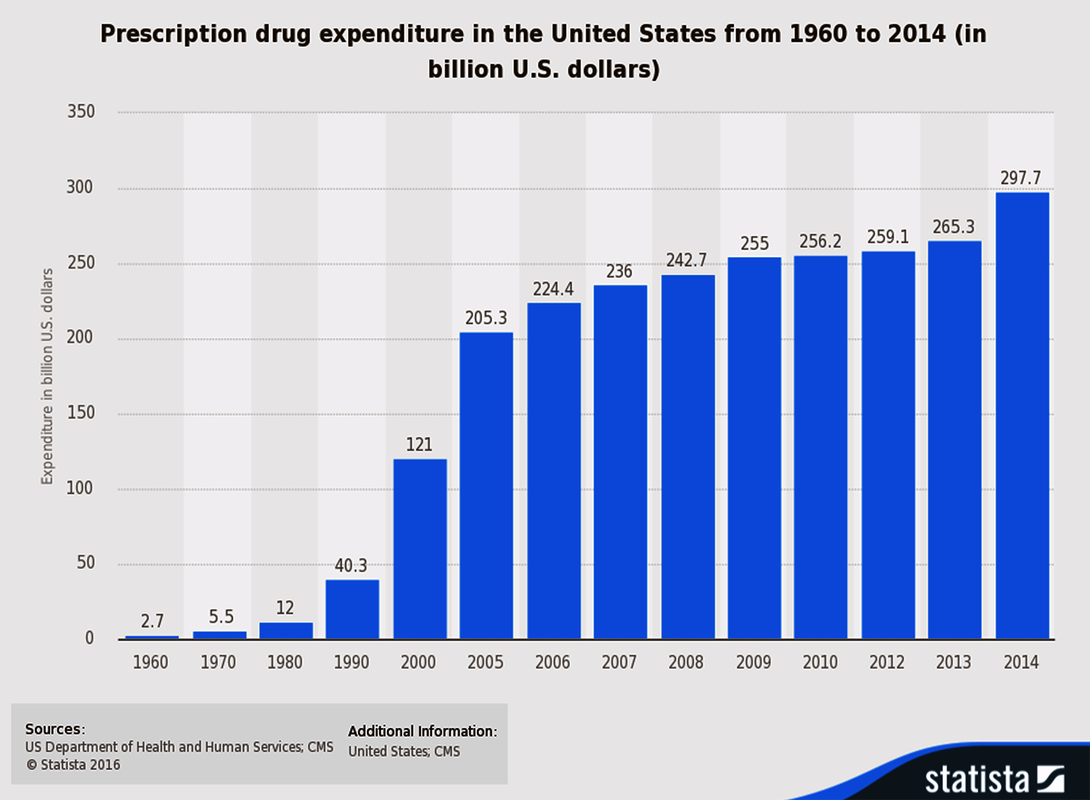

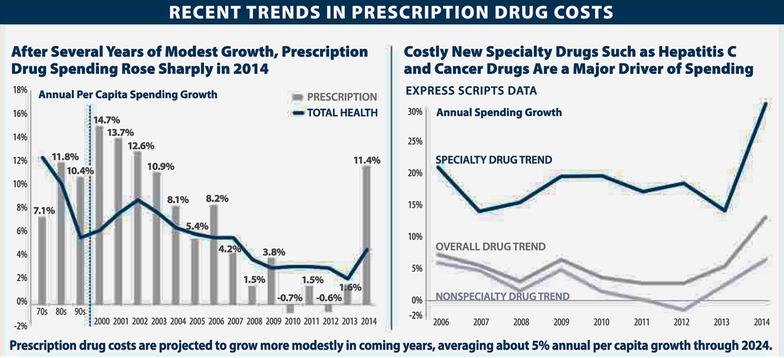

Undoubtedly, with the cost of Health Insurance Coverage going up more than 200-percent over the last 45 years (1970-2016), it is perhaps nearly as alarming to see that Prescription Drug Costs have similar skyrocketed 110-fold over the last 54 years from $2.7 billion to around $297.7 billion in national expenditures in 2014, according to The Centers for Medicare and Medicaid Services and Statista. Like the rest of American healthcare, a bulk of those increases are due a complete LACK of any U.S. federal regulation and any meaningful regulated “pricing controls” and “standardized pricing guidelines” explored in the previous chart above.

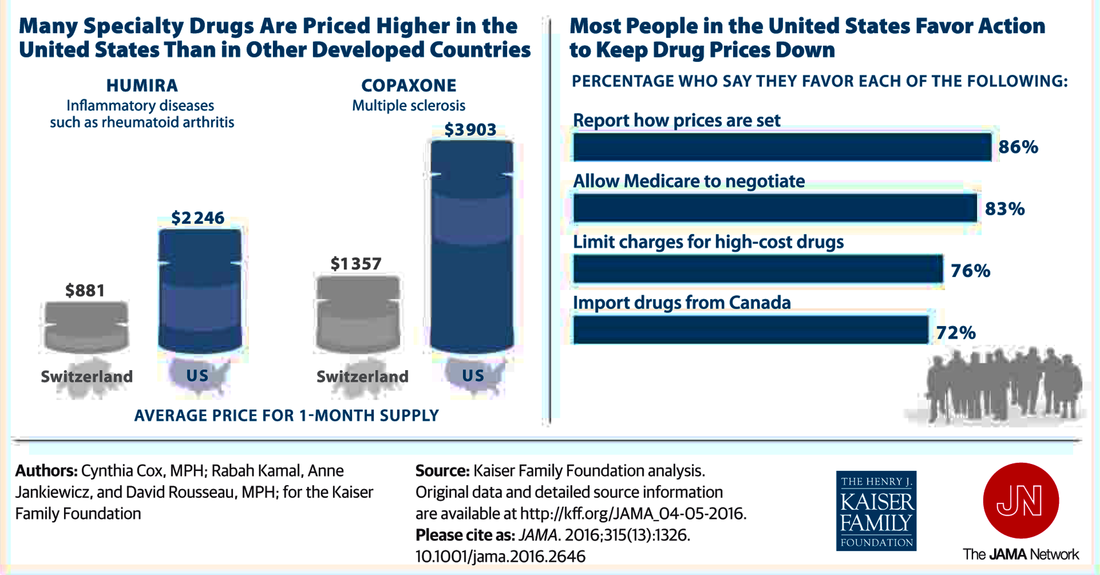

Much of the upward pressure on pricing is due so-called Big Pharma corporations striving for sometimes obscenely “optimum premium pricing” for greatly driving the annual U.S. spending growth rates (upwards of 30-percent in 2014 alone) with the burgeoning emphasis on “Specialty Drugs,” according to the Kaiser Family Foundation charts above and below.

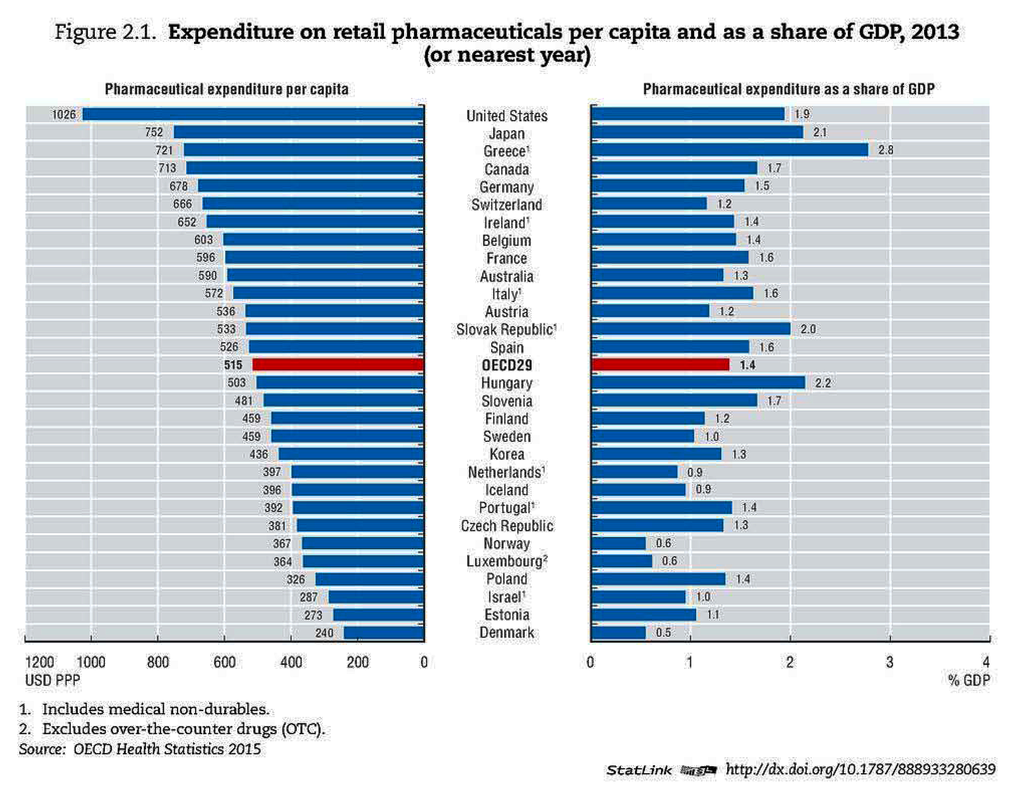

Seeking to be a “world leader” again for allowing “obscene profit exploitation,” the United States – predictably – also leads 39 nations of the Organization of Economic Cooperation and Development in the expenditure on “retail pharmaceuticals” per-capita at $1,026 in 2013. That is still 36-percent higher than the next nation, Japan ($752), but most telling is almost exactly DOUBLE than the 39-nation OECD average of $515. The typical response from Big Pharma conglomerates, particularly those based in the U.S., is that Americans typically pay more because a bulk of the “research and development” and meeting the clinical trials for “FDA approvals” are additional cost factors in getting new, experimental drugs to the U.S. marketplace.

Given that most employer-sponsored group health plans do not often include a full-coverage Dental Insurance Plan as well for employees, the financial burdens from ever-escalating dentistry costs coming out-of-pocket from workers just adds to the mounting woes over higher general health and pharmaceutical cost burdens on Americans of all economic classes. Perhaps, if there are “answers” to be found out of our growing “American healthcare crisis” gripping this country, it would come from looking at “working models” of “Social Health Maintenance Organizations” and “Nonprofit-based Community Health Plans” -- some of these operating successfully within Seniors-based (65-and-over) Medicare Advantage “supplemental health coverage” and the others in the general (65-and-under) Medicaid “expansion” or commercial marketplaces.

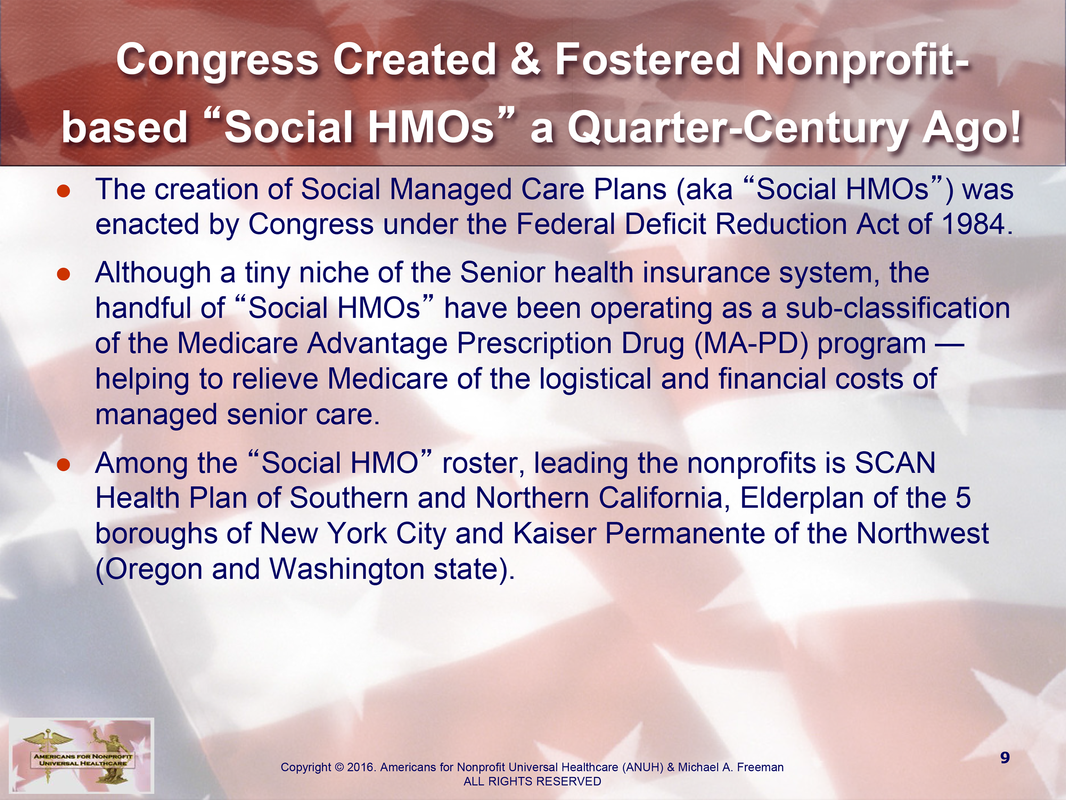

One of the best-kept secrets of American healthcare and representing a tiny sliver of the Medicare Advantage program are several nonprofit-based “Social Managed Care Plans” (aka “Social HMOs”) supplemental coverage plans serving Seniors. Operating within a special Medicare Advantage Part-D (aka “MA-PD”) segment of Medicare’s Part-D “prescription Part-D coverage option”are four of these Social Managed Care Plan organizations — SCAN Health Plan of California, Arizona and Nevada; Elderplan of Brooklyn, New York, and other surrounding boroughs of New York City; Kaiser Health Foundation of the Northwest (Portland-Vancouver metropolitan area, Salem, Ore., and Longview, Wash.), and Health Plan of Nevada of Las Vegas — that secured MA-PD funding from Medicare in servicing several hundred thousand Seniors with broad inpatient/outpatient and preventive health insurance coverage in their respective regions.

One of the best-kept secrets of American healthcare and representing a tiny sliver of the Medicare Advantage program are several nonprofit-based “Social Managed Care Plans” (aka “Social HMOs”) supplemental coverage plans serving Seniors. Operating within a special Medicare Advantage Part-D (aka “MA-PD”) segment of Medicare’s Part-D “prescription Part-D coverage option”are four of these Social Managed Care Plan organizations — SCAN Health Plan of California, Arizona and Nevada; Elderplan of Brooklyn, New York, and other surrounding boroughs of New York City; Kaiser Health Foundation of the Northwest (Portland-Vancouver metropolitan area, Salem, Ore., and Longview, Wash.), and Health Plan of Nevada of Las Vegas — that secured MA-PD funding from Medicare in servicing several hundred thousand Seniors with broad inpatient/outpatient and preventive health insurance coverage in their respective regions.

The longest running of these “Social HMOs” is the not-for-profit SCAN Health Plan (www.scanhealthplan.com), otherwise known as the Senior Care Action Network, founded in 1977 by a group of Long Beach, Calif. area seniors angered about some short-comings in the elder healthcare sector. With the backing and help of area doctors and other medical/caregiver practitioners joining their management staff, SCAN secured its first MA-PD funding from Medicare to offers health insurance and seniors-based healthcare services in 1985.

Today, SCAN provides insurance coverage and other wellness/preventive healthcare services to over 170,000 seniors in the Southern and Northern Californian regions, Arizona and Nevada. Over the last few years, SCAN has expanded its nonprofit services to senior residents of Maricopa County (Phoenix) in Arizona and in Northern California — nearly doubling its number of Senior subscribers over the last half-dozen years. One of the proud hallmarks of SCAN is that they typically average 4.5 stars in “quality of care” surveys conducted by Medicare.

In Southern California, for example, a key ingredient of SCAN’s success is its broad area roster of 17,000-plus registered “in-network” doctors and specialists and over 200 hospital choices. SCAN’s care menu is so broad and comprehensive, it includes other types of “Special Needs” in-patient hospital care; out-patient doctor/hospital care; at-home care; emergency admittance and transportation services coverage; a prescription brand/generic drug program; vision services; dental coverage; hearing; other no- to low-cost co-pays on a variety of screenings and exams; and a wide array of preventive and health-and-wellness services — features necessary for senior care but MUCH GREATER than what could be found in either standard Medicare and so-called “Cadillac Plans” from PRIVATE/FOR-PROFIT insurance carriers either similarly participating in the Medicare Advantage (Part A & B) programs or for the general under-65 population as well.

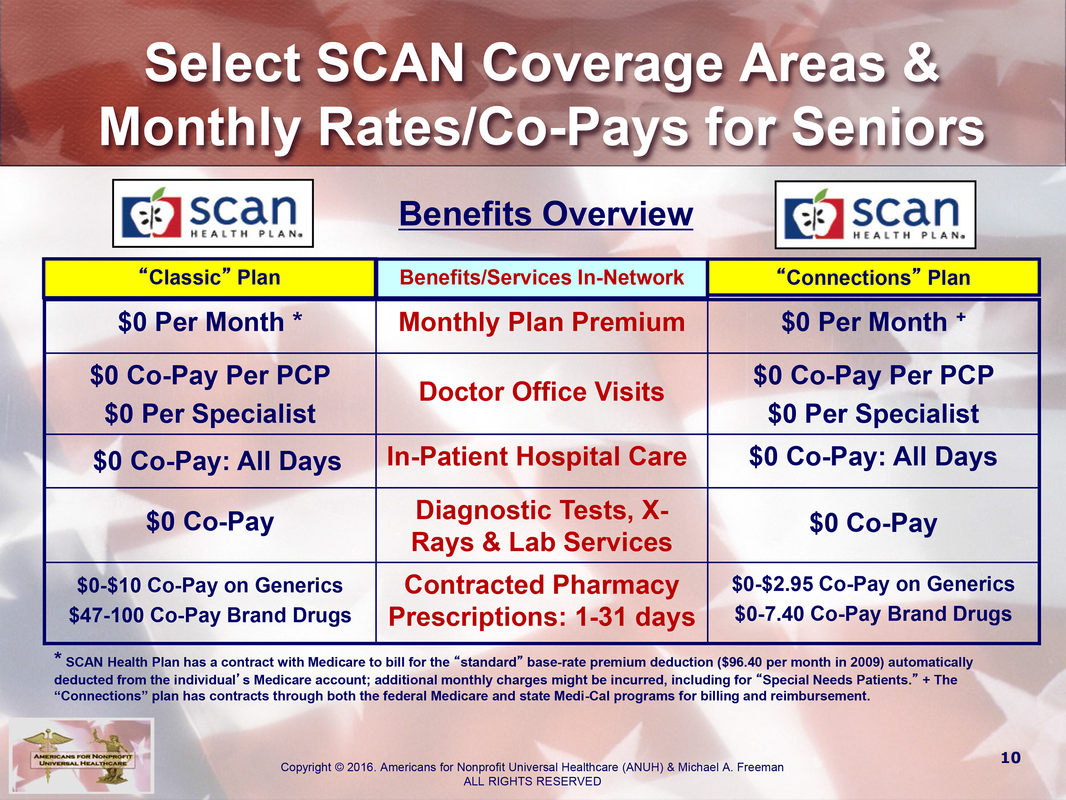

Most notably, out-of-pocket costs, or so-called co-pay expenses to senior subscribers, come at mere fractions in two of SCAN Health Plan’s choices — “Classic” and “Connections” plans. “Connections” is offered for “Special Needs Plans,” which are offered (under Medicare Advantage guidelines) to Seniors who have long-term chronic illnesses/diseases, reside in special advanced care institutions (like a nursing home) and require a broader array of drug formularies coverage.

In Southern California, for example, a key ingredient of SCAN’s success is its broad area roster of 17,000-plus registered “in-network” doctors and specialists and over 200 hospital choices. SCAN’s care menu is so broad and comprehensive, it includes other types of “Special Needs” in-patient hospital care; out-patient doctor/hospital care; at-home care; emergency admittance and transportation services coverage; a prescription brand/generic drug program; vision services; dental coverage; hearing; other no- to low-cost co-pays on a variety of screenings and exams; and a wide array of preventive and health-and-wellness services — features necessary for senior care but MUCH GREATER than what could be found in either standard Medicare and so-called “Cadillac Plans” from PRIVATE/FOR-PROFIT insurance carriers either similarly participating in the Medicare Advantage (Part A & B) programs or for the general under-65 population as well.

Most notably, out-of-pocket costs, or so-called co-pay expenses to senior subscribers, come at mere fractions in two of SCAN Health Plan’s choices — “Classic” and “Connections” plans. “Connections” is offered for “Special Needs Plans,” which are offered (under Medicare Advantage guidelines) to Seniors who have long-term chronic illnesses/diseases, reside in special advanced care institutions (like a nursing home) and require a broader array of drug formularies coverage.

For example, an in-hospital stay of 1 day to 150 days incurs out-of-pocket costs of up to $2,300 under the standard Medicare plan while SCAN’s “Classic” and the “Connections” plan hospital days and feature ZERO ($0) $0 co-pay deductibles for unlimited stays. In fact, if you peruse either of SCAN’s two plans (on http://www.ScanHealthPlan.com), most of the benefit categories feature $0 co-pays/deductibles and hit a maximum of $100 for select care services. Co-pays for pharmaceutical prescription drugs are “zero” to “low-cost” on Generic Drugs while ranging up to $7.40 to $47-$100 maximum for Brand-name Drugs under SCAN’s “Connections” and “Classic” plans, respectively. In all, a SCAN premium holder will pay an annual “maximum out-of-pocket” (MOOP) expense of $2,000 annually under the “Classic” plan.

Perhaps the most intriguing figure comes from a Wikipedia.org estimate that SCAN earns $1.9 billion in revenue from its direct reimbursement billings to Medicare, which translates to a premium cost of up to $103 per month for each of its 170,000 subscribers or $1,236 per year for its full array of covered services — although Medicare’s database factors in the potential additional surcharge of up to $56 per month for SCAN’s Special Needs Plan (SNP) subscribers and other “options-based” premium charges.

Perhaps the most intriguing figure comes from a Wikipedia.org estimate that SCAN earns $1.9 billion in revenue from its direct reimbursement billings to Medicare, which translates to a premium cost of up to $103 per month for each of its 170,000 subscribers or $1,236 per year for its full array of covered services — although Medicare’s database factors in the potential additional surcharge of up to $56 per month for SCAN’s Special Needs Plan (SNP) subscribers and other “options-based” premium charges.

Better yet, the most startling fact in this is that SCAN and the other major NONPROFIT health insurance carriers participating in the MA-PD program provide much higher levels of premium coverage and at lower co-pay/deductible costs and “in-Medicare” monthly premium fees ($96 per month in 2009) — at about one-fifth (20%) to one-quarter (25%) of the cost of an average $400 to $500 per month (or $4,800 per-year premium average) of what FOR-PROFIT/PRIVATE health insurance carrier charges on a premium for an individual policyholder in the general under-65 population, according to World Health Organization data.

If FOR-PROFIT/PRIVATE health insurance carriers can so boldly market their so-called top-of-the-line plans as “Cadillac Premiums,” than several nonprofit “Social HMOs” including SCAN’s Medicare-based plans for seniors should be coined the “Rolls-Royce Premiums” of health insurance. It just proves that a greatly expanded menu of benefits and lower deductibles and co-pays are very achievable at a fraction of the monthly/yearly costs of what FOR-PROFIT/PRIVATE health insurers offer.

If you are a Senior or nearing the age of 65, there is an online directory of Medicare Advantage plans (at https://www.medicare.gov/find-a-plan/questions/home.aspx) listed on a state-by-state and plan-specific basis, which reveals a convenient database for searching out a wide array of mostly FOR-PROFIT/PRIVATE health insurance carriers that offer senior “option” plans. Some of the plans are sponsored by the American Association of Retired People (AARP), but they originate from FOR-PROFIT, pay subscription plans (outside of standard Medicare-provided health insurance) typically featuring considerably higher co-pays/deductibles and far fewer coverage areas. ANUH has also embedded below a “Directory of NONPROFIT-based Medicare Advantage Plans” from across the country (about 300 in all).

If FOR-PROFIT/PRIVATE health insurance carriers can so boldly market their so-called top-of-the-line plans as “Cadillac Premiums,” than several nonprofit “Social HMOs” including SCAN’s Medicare-based plans for seniors should be coined the “Rolls-Royce Premiums” of health insurance. It just proves that a greatly expanded menu of benefits and lower deductibles and co-pays are very achievable at a fraction of the monthly/yearly costs of what FOR-PROFIT/PRIVATE health insurers offer.

If you are a Senior or nearing the age of 65, there is an online directory of Medicare Advantage plans (at https://www.medicare.gov/find-a-plan/questions/home.aspx) listed on a state-by-state and plan-specific basis, which reveals a convenient database for searching out a wide array of mostly FOR-PROFIT/PRIVATE health insurance carriers that offer senior “option” plans. Some of the plans are sponsored by the American Association of Retired People (AARP), but they originate from FOR-PROFIT, pay subscription plans (outside of standard Medicare-provided health insurance) typically featuring considerably higher co-pays/deductibles and far fewer coverage areas. ANUH has also embedded below a “Directory of NONPROFIT-based Medicare Advantage Plans” from across the country (about 300 in all).

During the original Healthcare Reform debates in Washington (from 2009-2010), two previous incarnations of our ANUH advocacy organization -- Trans-American Alliance for a National Consensus (TANC) and Americans for a Nonprofit Health Insurance Exchange (ANHPIE) -- released the following presentation video, “Rx for U.S. Healthcare Reform,” exploring the same kind of “profit exploitation-based marketplace dynamics” besieging American healthcare for more than a century now.

Some of the data and structural points about American healthcare, particularly since the later 2014 rollout of the “state-run marketplace insurance exchanges” of ACA/Obamacare became a reality, may appear dated; but if you have under an hour to spare, the video presentation below gives you a picture of the outstanding “working models” of NONPROFIT-based “Social HMOs” of the Medicare Advantage Part-D program as well as locally-rooted “Nonprofit Community Health Plans” that operate today around the country.

Some of the data and structural points about American healthcare, particularly since the later 2014 rollout of the “state-run marketplace insurance exchanges” of ACA/Obamacare became a reality, may appear dated; but if you have under an hour to spare, the video presentation below gives you a picture of the outstanding “working models” of NONPROFIT-based “Social HMOs” of the Medicare Advantage Part-D program as well as locally-rooted “Nonprofit Community Health Plans” that operate today around the country.

More than anything, the fact is the NONPROFIT-based “Social HMOs” participating in the Medicare Advantage Part-D program deliver so much more health coverage for much less cost (seems unbelievable given America’s long-standing “profit-obsessive marketplace patchwork,” huh?!), is all the more reason why our country needs to embrace “Nonprofit Community Health Plans” in the broader under-65 marketplace as well. The fact is that achieving a “Medicare For All” universal healthcare vision that Sen. Bernie Sanders will take a Herculean legislative effort (especially getting Obamacare repeal-crazed Republicans on board), but it could be done by simply marrying Medicare with Obamacare’s expanding Medicaid services (for lower-income, under-65 adults) yet fostering new FEDERAL backing and funding of “Nonprofit Community Health Plans” would be a natural “steppingstone” pathway move to full Single-Payer Universal Healthcare.

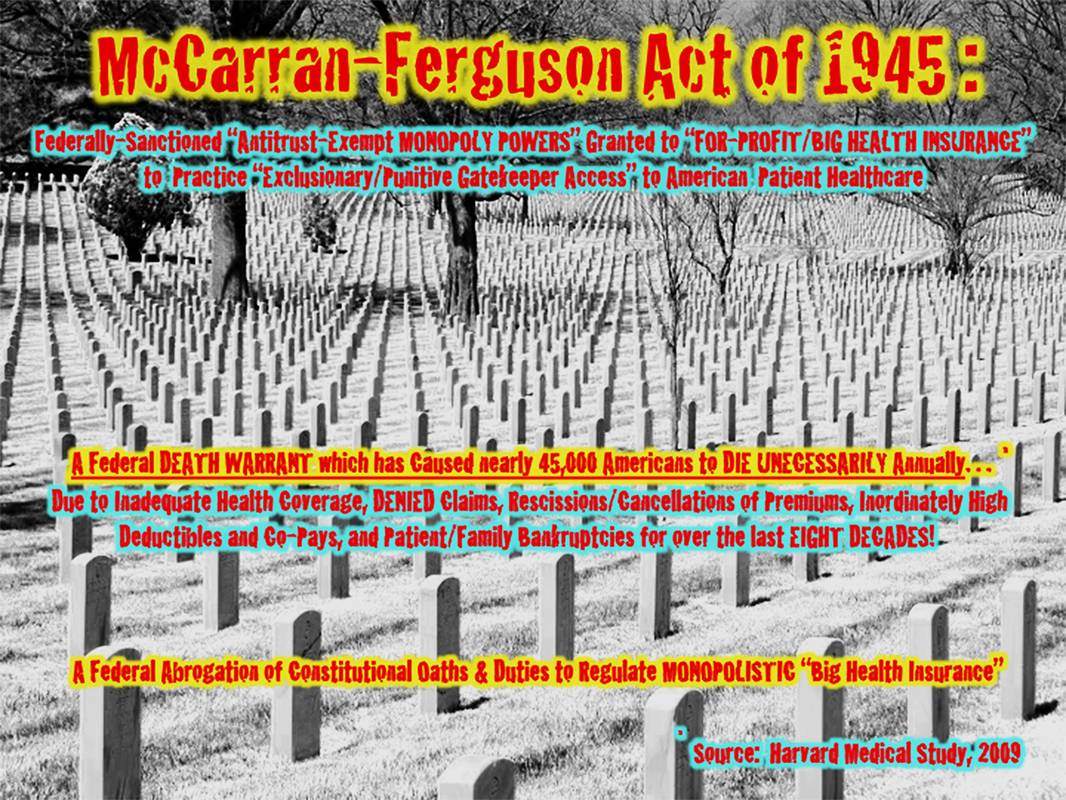

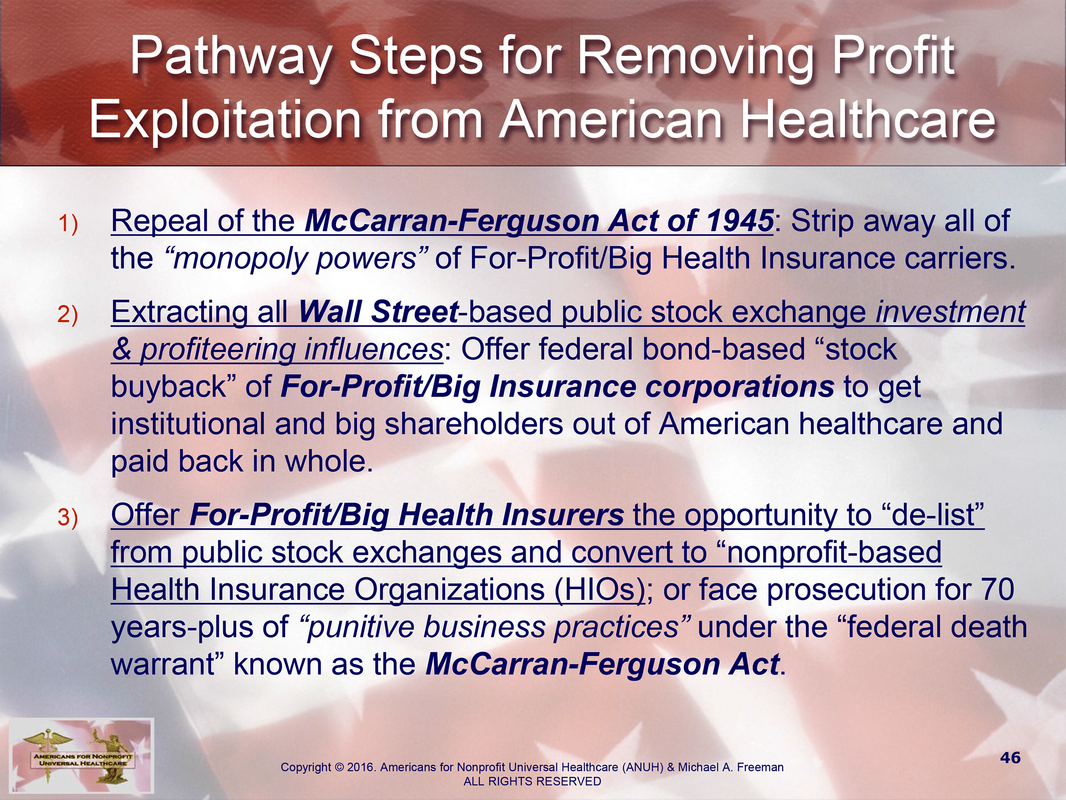

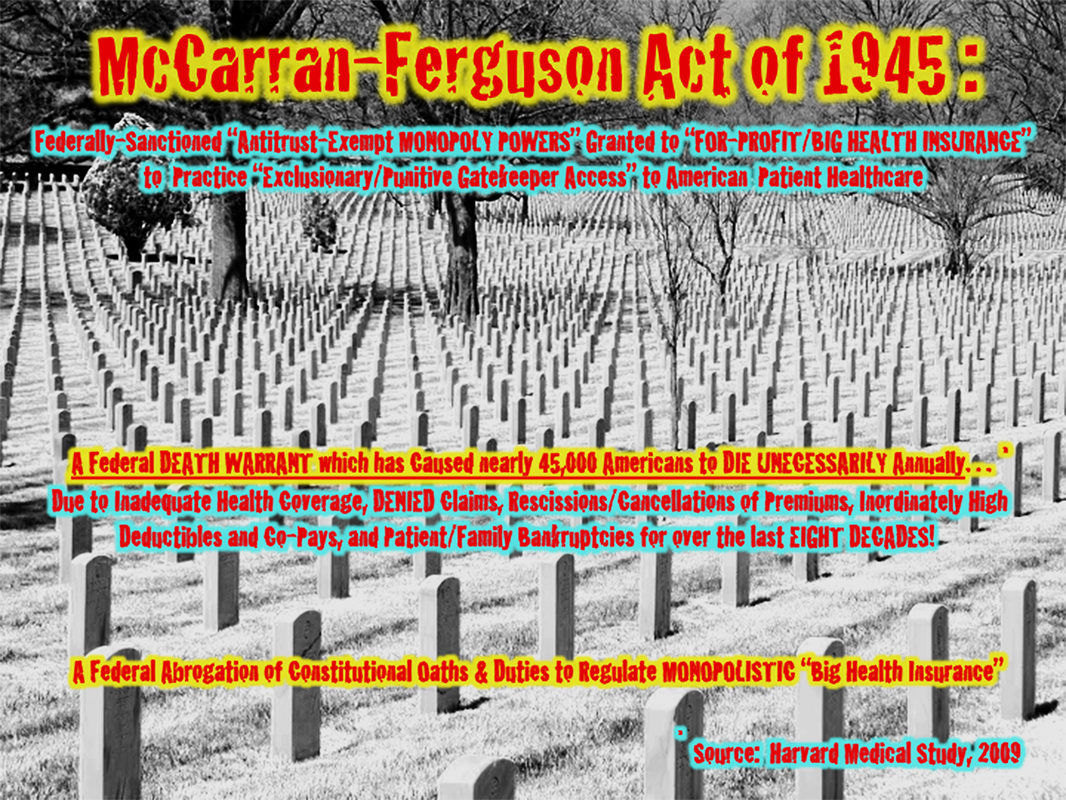

Stemming all the way back to the founding roots of American healthcare during Colonial Times (from the 18th to 19th centuries), NONPROFIT-based ecumenical and community health care organizations were the predominant providers of medical treatment…well, until the country’s labor unions began offering healthcare services to their members through “private insurance plans.” From about the turn of the 20th Century, the economic and legislative tides tilted massively in favor of the For-Profit/Big Health Insurance carriers — formally cementing into place a highly-unusual, hugely-punitive “antitrust-exempt” status from the federal government for Big Health Insurance to form UNREGULATED MONOPOLIES, thanks to Congress passing the McCarran-Ferguson Act of 1945.

Stemming all the way back to the founding roots of American healthcare during Colonial Times (from the 18th to 19th centuries), NONPROFIT-based ecumenical and community health care organizations were the predominant providers of medical treatment…well, until the country’s labor unions began offering healthcare services to their members through “private insurance plans.” From about the turn of the 20th Century, the economic and legislative tides tilted massively in favor of the For-Profit/Big Health Insurance carriers — formally cementing into place a highly-unusual, hugely-punitive “antitrust-exempt” status from the federal government for Big Health Insurance to form UNREGULATED MONOPOLIES, thanks to Congress passing the McCarran-Ferguson Act of 1945.

During the 70-plus years of McCarran-Ferguson’s torturous existence, it had been estimated in a 2009 Harvard Medical study that 45,000 Americans died unnecessarily annually due to a ”lacking adequate levels of health insurance coverage or having none at all.” Essentially, under McCarran-Ferguson, the federal government abrogated most oversight of the insurance industries, allowing the For-Profit/Big Health Insurance carriers to come under the states’ regulation, which typically is lax or nonexistent with most “state insurance commissions” seated by former insurance industry executives.

Even though the federal passage of the Affordable Care Act in 2010 set mandates to ban the insurance industry’s one-time practice of “rescinding/cancelling premiums” for people discovered with “preexisting medical conditions,” there have still been widespread reports of For-Profit/Big Insurance carriers back to “denying claims” on some routine diagnostic and major experimental surgical procedures (as discussed in Part III of this blog). And as such major For-Profit Health Insurers as UnitedHealthGroup and Humana, among others, hinting at “product exits” from the federally-backed “ACA state healthcare insurance exchanges” by 2017, these still-very profitable companies are threatening the near-term viability of the so-called Obamacare national “health safety net” that had been built up since 2014.

Bottom-line what America has witnessed is how millions — likely billions -- of Americans have suffered and died unnecessarily from the 1) punitive business practices; 2) artificial price manipulations; 3) monopolizing of local markets across the country; 4) unfair/anticompetitive business activities, market allocations and collusion; 5) and out-of-pocket cost burden shifting onto consumers conducted by For-Profit/Big Insurance Carriers for over eight decades…and counting. For those reasons (and others), these For-Profit/Big Health Insurance Carriers have violated any number of federal statutes pertaining to criminal business practices (not mention to possible murder charges for denials of claims and rescissions of premiums for consumers awaiting life-saving treatments, but later died in the interim) and now looking to strangle Obamacare into repeal, they do not deserve any right to hold business licenses to serve the public as “for-profit” entities.

- Michael A. Freeman

Even though the federal passage of the Affordable Care Act in 2010 set mandates to ban the insurance industry’s one-time practice of “rescinding/cancelling premiums” for people discovered with “preexisting medical conditions,” there have still been widespread reports of For-Profit/Big Insurance carriers back to “denying claims” on some routine diagnostic and major experimental surgical procedures (as discussed in Part III of this blog). And as such major For-Profit Health Insurers as UnitedHealthGroup and Humana, among others, hinting at “product exits” from the federally-backed “ACA state healthcare insurance exchanges” by 2017, these still-very profitable companies are threatening the near-term viability of the so-called Obamacare national “health safety net” that had been built up since 2014.

Bottom-line what America has witnessed is how millions — likely billions -- of Americans have suffered and died unnecessarily from the 1) punitive business practices; 2) artificial price manipulations; 3) monopolizing of local markets across the country; 4) unfair/anticompetitive business activities, market allocations and collusion; 5) and out-of-pocket cost burden shifting onto consumers conducted by For-Profit/Big Insurance Carriers for over eight decades…and counting. For those reasons (and others), these For-Profit/Big Health Insurance Carriers have violated any number of federal statutes pertaining to criminal business practices (not mention to possible murder charges for denials of claims and rescissions of premiums for consumers awaiting life-saving treatments, but later died in the interim) and now looking to strangle Obamacare into repeal, they do not deserve any right to hold business licenses to serve the public as “for-profit” entities.

- Michael A. Freeman

MORE TK COME...TK...

RSS Feed

RSS Feed