Even a few years into so-called “Obamacare” (and the federal enactment of The Patient Protection and Affordable Care Act of 2010) in what could be simplified as an expansion of Medicaid (for indigent Americans under 65 years of age), “mandated” health coverage and state- or federally-run Health Insurance Exchanges, it is the national consternation and conflicting interests of large antitrust-exempt “For-Profit/Big Health Insurance Carriers” that seemingly make accessible Universal Healthcare an unattainable, “bridge-too-far” proposition for America to cross…or possibly embrace.

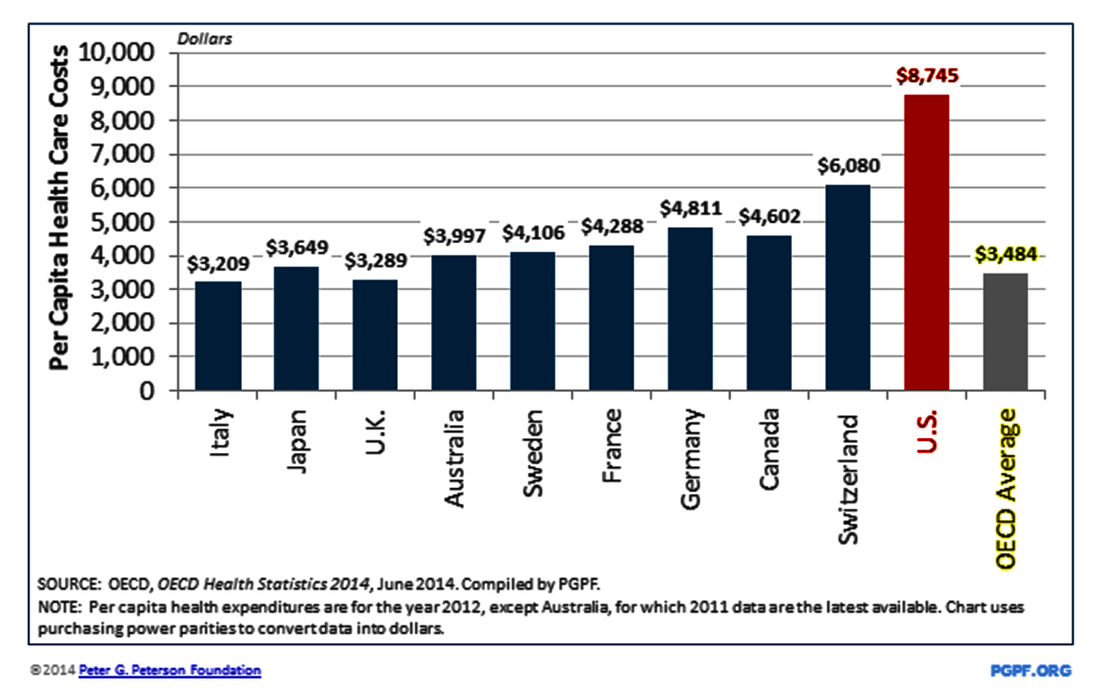

After all, these For-Profit Big Healthcare and Wall Street- and Washington-based “special interests” want to preserve a “marketplace- and monopoly-dictated healthcare patchwork” that saddles America with a world-leading and ever-spiraling $3.3 TRILLION in annual expenditures, gobbling up over 17 percent of our nation’s Gross Domestic Product (GDP). What this translates to is Americans paying about $9,000 per-capita for healthcare in the USA – almost 50-percent higher than the next highest nation (Switzerland) and about THREE TIMES more than the average ($3,484) among nine of the Organization for Economic Cooperation and Development (OECD) nations with Universal Healthcare systems listed in the bar chart below.

After all, these For-Profit Big Healthcare and Wall Street- and Washington-based “special interests” want to preserve a “marketplace- and monopoly-dictated healthcare patchwork” that saddles America with a world-leading and ever-spiraling $3.3 TRILLION in annual expenditures, gobbling up over 17 percent of our nation’s Gross Domestic Product (GDP). What this translates to is Americans paying about $9,000 per-capita for healthcare in the USA – almost 50-percent higher than the next highest nation (Switzerland) and about THREE TIMES more than the average ($3,484) among nine of the Organization for Economic Cooperation and Development (OECD) nations with Universal Healthcare systems listed in the bar chart below.

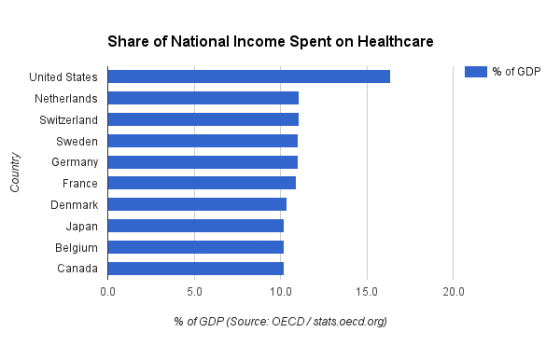

What is the most illustrative of the virtual lack of federal government regulation on the “for-profit/publicly-traded corporations” dominating the American healthcare marketplace is the ever-skyrocketing costs of the middleman-based, antitrust-exempt “Big Health Insurance” and the Big Pharmaceuticals industries, in particular. Overall, with national healthcare spending eating up just over 17-percent of America’s GDP, the U.S. is typically 50- to 70-percent higher than other “Universal Care-served nations.”

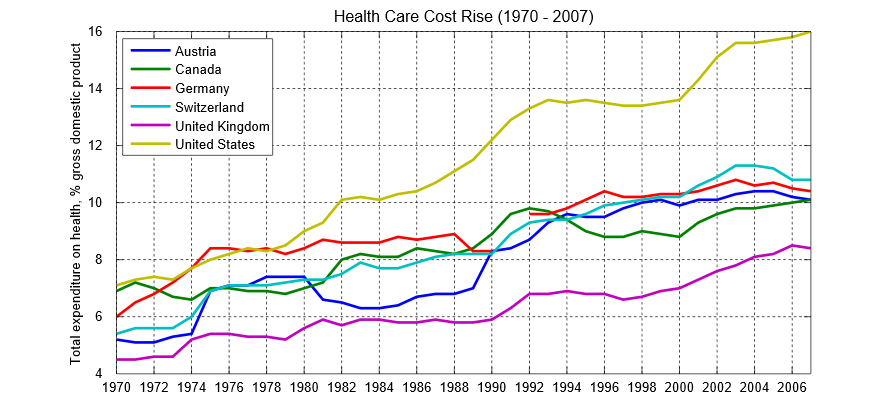

Most alarmingly, since 1970, America has seen the cost of healthcare skyrocket almost 300-percent from 46 years ago (at roughly 7-percent of GDP back in 1970) to just over 17-percent today while the OECD nations – including Canada and Australia, along with several Western European nations – have been much more effective maintaining government-regulated “pricing controls” and a mix of government-/privately-financed Universal Healthcare systems effectively moderating medical practitioner, hospital and pharma costs, thus keeping their GDP costs to just around the 10-percent threshold in most cases.

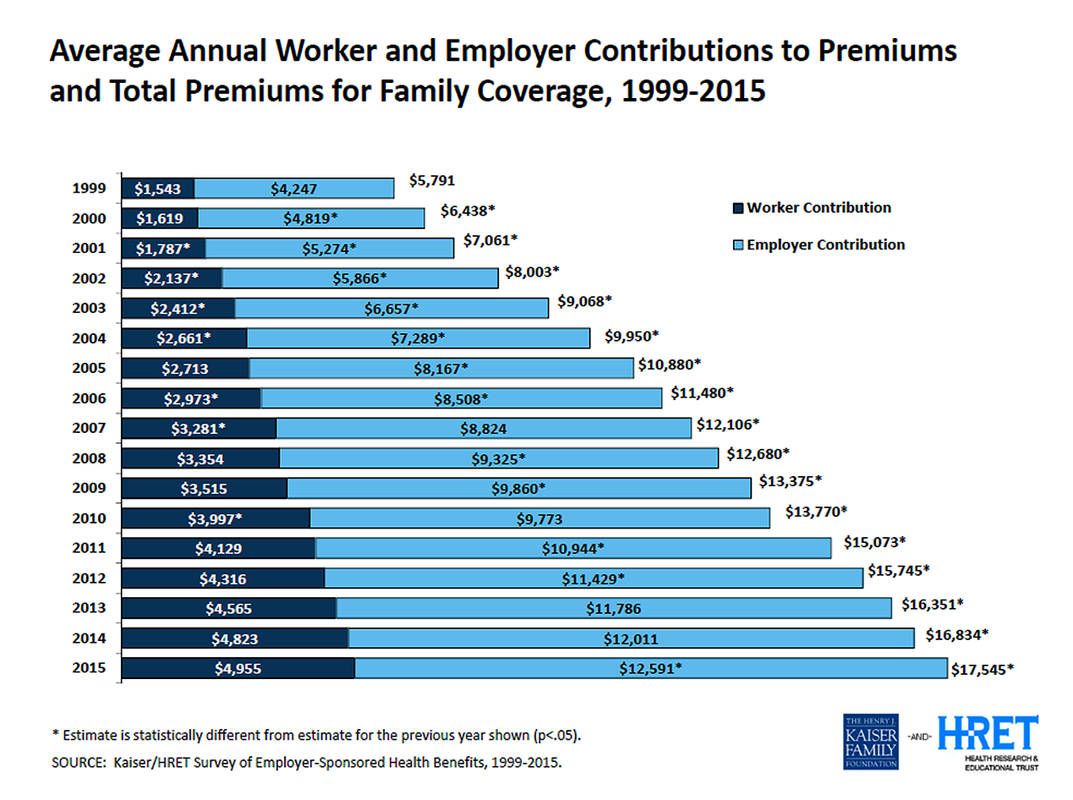

2014 marked the inaugural year of the “state-run” insurance exchanges and Healthcare.gov-backed federal “marketplace” exchanges (the latter in states which did NOT enact state-based exchanges). What is readily apparent is that the annual pricing increases in “Family Coverage” insurance premiums leveled off from the launch of the Obamacare-originated exchange structure as noted in the chart below (courtesy of The Kaiser Family Foundation and Health Research and Educational Trust data).

The $17,545 average for a “family” premium in 2015 represented a smaller 4-percent increase from the previous $16,834 average in 2014. But if you go back to 2010, when Congress had at first passed the Affordable Care Act into law, the average “family” health insurance premium came with a $13,770 average, followed by a 9 percent annual increase to $15,073. The first year of the Healthcare.gov and state-run exchanges in 2014 did slow annual growth to 4 percent from the 2013 average of $16,351. (It is also interesting to note that the total cost of a family premium in 1999 [$5,791] has risen a whopping 203-percent over the course of 16 years to $17,545 for 2015).

The $17,545 average for a “family” premium in 2015 represented a smaller 4-percent increase from the previous $16,834 average in 2014. But if you go back to 2010, when Congress had at first passed the Affordable Care Act into law, the average “family” health insurance premium came with a $13,770 average, followed by a 9 percent annual increase to $15,073. The first year of the Healthcare.gov and state-run exchanges in 2014 did slow annual growth to 4 percent from the 2013 average of $16,351. (It is also interesting to note that the total cost of a family premium in 1999 [$5,791] has risen a whopping 203-percent over the course of 16 years to $17,545 for 2015).

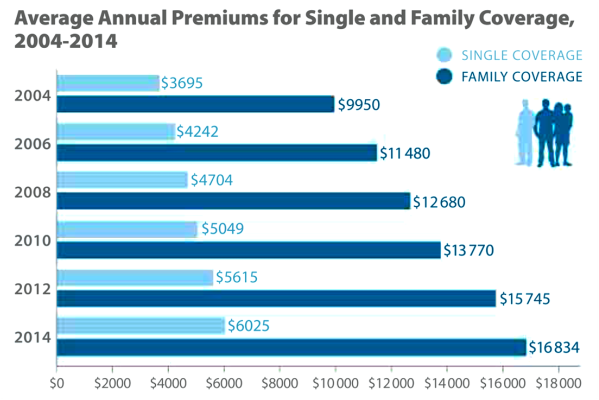

Between the 2012 and 2014 years, “individual/single” health insurance premiums also increased 7-percent from a $5,615 to $6,025 annual average cost in those respective years, according to a Kaiser Family Health Foundation and Journal of American Medicine study (below). But the preceding 2010-to-2012 span marked a somewhat larger 11-percent “pre-exchange” pricing increase — so, in some ways, Obamacare has been successful in reducing the pricing hikes, but it has been more recently reported that the For-Profit/Big Health Insurers are already hinting at bigger increases in 2017 because some of them claim they are losing money on the Healthcare.gov and state-run exchanges.

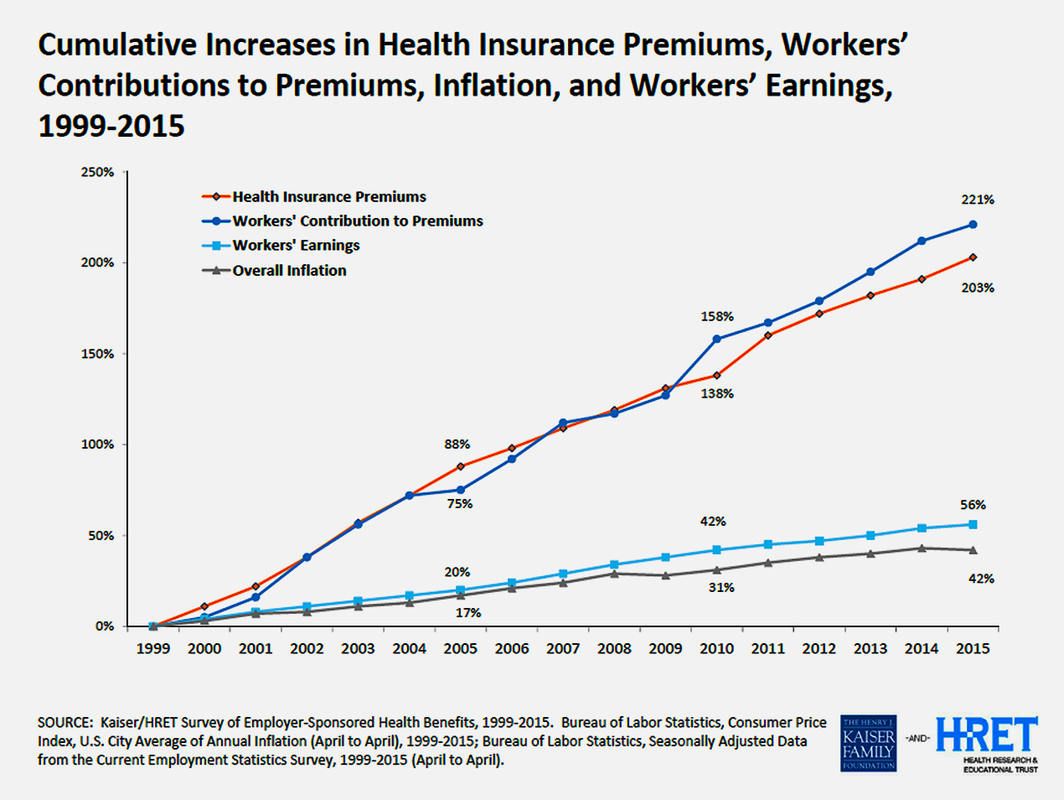

Most decidedly alarming, though, is the indisputable, unyielding escalation in the cost of the “Family Coverage” as an ever-growing burden on both workers and employers. Over a span of 16 years, from 1999-2015, the cost of “Family Coverage” has skyrocketed by a cumulative 203-percent (from $5,791 annual average in 1999 to $17,545 in 2015), which marks an adjusted mean 12.7-percent annual average increase during the period, according to Kaiser Family Health and HRET research in the chart below. The pain, of course, is most acutely felt by American workers, whom have seen their wages increase by just 56-percent during the same 16-year period — translating to a mean 3.5-percent average annual increase in their earnings.

On top of employees seeing that their employer-endorsed family insurance increases outpacing their marginal annual salary increases by a roughly 160-percent margin hauled in by the “antitrust-exempt” For-Profit/Big Health Insurance industry over the decade-and-a-half span, employers have also asked their workers for ever-larger contributions to their group health plans. Employee contributions to employer-sponsored “family” health coverage plans increased 221-percent over the 16-year period cited in the KFF-HRET study — yet again translating to 13.8-percent mean annual increases in worker contributions from 1999-2015.

Whatever positve “halo effect” may be hoped from the enactment of the Affordable Care Act/Obamacare had no impact on how For-Profit/Big Health Insurers continued to somewhat more subversively shield “cost burden shifting onto the backs of American workers” in order for them to preserve and continue to grow certain levels of profitability for their “publicly-traded corporations” obsessively seeking to meet Wall Street “earnings expectations.” Most alarmingly the “burden-shifting strategy” employed by the For-Profit/Big Health Insurance monopolists not only centers on raising deductible levies on American consumers, it also applies to co-pay burdens additionally growing at an undocumented pace, too.

Whatever positve “halo effect” may be hoped from the enactment of the Affordable Care Act/Obamacare had no impact on how For-Profit/Big Health Insurers continued to somewhat more subversively shield “cost burden shifting onto the backs of American workers” in order for them to preserve and continue to grow certain levels of profitability for their “publicly-traded corporations” obsessively seeking to meet Wall Street “earnings expectations.” Most alarmingly the “burden-shifting strategy” employed by the For-Profit/Big Health Insurance monopolists not only centers on raising deductible levies on American consumers, it also applies to co-pay burdens additionally growing at an undocumented pace, too.

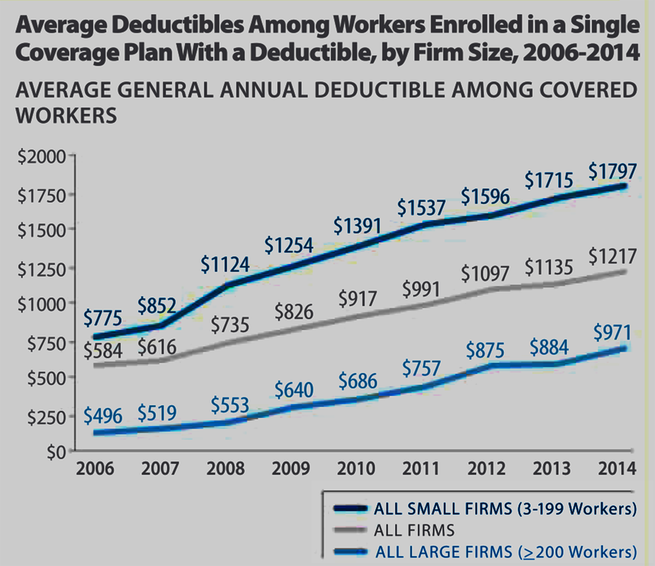

In the nine years of 2006-to-2014 for workers enrolled in “Single Coverage/Invidual” health coverage plans, the average of “deductibles” coming out of employees’ pockets among “all firms” (the middle, gray-colored line in the chart above) steadily climbed 108-percent from a $584 yearly average in 2006 to $1,217 annual cost in 2014. Predictably, among “small firms” with no more than 199 workers, the average cost of “out-of-pocket deductibles” rose by a whopping 131-percent from $775 yearly average in 2006 to $1,797 annual average in 2014, according to Kaiser Family Foundation and JAMA.

Essentially, American consumers cannot escape the facts they are “paying evermore for health insurance and getting less coverage in return by seeing that the burdens of deductibles and co-pays are being laden onto their shoulders like a cheerleader-diamond pile of 6 million-pound gorillas.” And the third major whammy middle- to upper-middle class American consumers face from the sausage-made “mandated” statutes of the Affordable Care Act are “individual tax penalties” if taxpayers “cannot show proof” of attaining health insurance coverage (either through an employer-sponsored group plan, the state-run/Healthcare.gov “insurance exchanges” or private/individual commercial means).

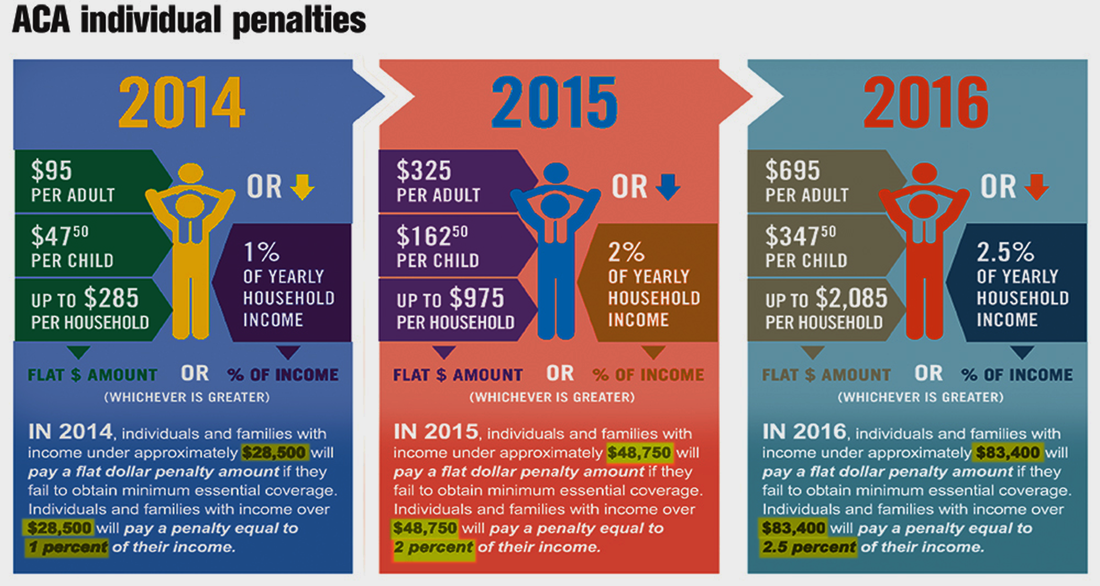

As the chart from ObamacareFacts.com lays out below, the ACA tax penalties started at $95 per-adult and up to $285 per-household levied on American taxpayers who did NOT file statements of proof with the Internal Revenue Service that they were in compliance with mandated health insurance coverage. In the most recently completed 2015 tax year, the individual penalties increased to $325 per-adult and up to $925 per-household fines. Starting in tax year 2016 in what U.S. Department of Health and Human Services (HHS) and U.S. Treasury Department have claimed will be a topped-out $695 per-adult and up to $2,085 per-household and will hold at that level for the foreseeable future.

As the chart from ObamacareFacts.com lays out below, the ACA tax penalties started at $95 per-adult and up to $285 per-household levied on American taxpayers who did NOT file statements of proof with the Internal Revenue Service that they were in compliance with mandated health insurance coverage. In the most recently completed 2015 tax year, the individual penalties increased to $325 per-adult and up to $925 per-household fines. Starting in tax year 2016 in what U.S. Department of Health and Human Services (HHS) and U.S. Treasury Department have claimed will be a topped-out $695 per-adult and up to $2,085 per-household and will hold at that level for the foreseeable future.

For the 2014 tax year, the IRS estimated that 7.5 million taxpayers — in non-compliance with the ACA “mandate” to obtain health coverage — paid an “average” $200 tax penalty. That would mean the IRS collected a total of roughly $1.5 billion in ACA tax penality revenues nationally. Under the dense, somewhat Byzantine language of the Affordable Care Act, the money raised from tax penalties is allegedly allocated for the continuing expansion of Medicaid (to Americans qualifying at 138-percent or below the “Federal Poverty Level” [FPL] for federal government-back health coverage); tax subsidies for Americans buying into the state- and Healthcare.gov-run insurance exchanges; Medicare coverage for Seniors 65-years-and-over; and the funding of other state and federal health plans.

Nevertheless, there are widespread Social Network-generated stories, blogs and chat threads suggesting more and more Americans — even those low- to middle-income-bracket taxpayers within the 138-percent to 400-percent of Federal Poverty Levels who “qualify” for ACA/Obamacare “tax subsidies” to buy coverage within or outside the state- and federal-run insurance exchanges — are hinting they will either pay the fines or simply decline to file their federal income taxes because they still cannot afford the subsidized insurance exchange plans.

The business cable TV network, CNBC, reported in July 2015 that 12 million Americans (those extensively rumored to be hovering between the 138- to 400-percent FPL) successfully received “exemptions” from the ACA mandate tax penalties. That represented 9-percent of all filers, reported CNBC, which noted earlier Congressional Budget Office projections were for upwards of 20-percent of all filers seeking “exemptions.”

Perhaps, most perplexing is CNBC reporting upwards of 5.1 million Americans “failed to state they had health coverage, or say they had paid the fine, citing unnamed “IRS officials.” The network reported that the IRS is now “analyzing these cases to determine their status,” according to a letter IRS officials sent to Congress.

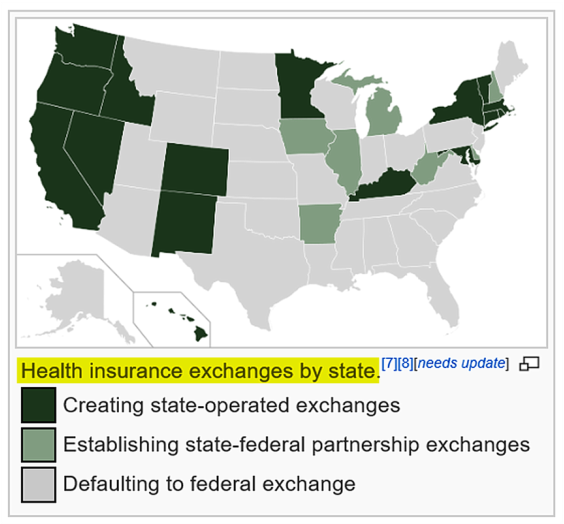

The cloudy status of some taxpayers who have potentially become Obamacare/ACA “mandate scofflaws” (in some cases) was originally the anticipated source and point of contention between the 27 states which filed to sue the federal government over the “Constitutionality” of “mandated” healthcare coverage. The number of states filing lawsuits also coincided with the states graphically depicted in the chart below (from Wikiepedia.org) which declined federal funding for creating “state-run insurance exchanges” (instead “defaulting” to the federally-run Healthcare.gov exchanges) and conversely refusing federal funding for expansions of Medicaid coverage for the poor-to-low-income Americans at the 138-percent and below Federal Poverty Line for coverage).

The business cable TV network, CNBC, reported in July 2015 that 12 million Americans (those extensively rumored to be hovering between the 138- to 400-percent FPL) successfully received “exemptions” from the ACA mandate tax penalties. That represented 9-percent of all filers, reported CNBC, which noted earlier Congressional Budget Office projections were for upwards of 20-percent of all filers seeking “exemptions.”

Perhaps, most perplexing is CNBC reporting upwards of 5.1 million Americans “failed to state they had health coverage, or say they had paid the fine, citing unnamed “IRS officials.” The network reported that the IRS is now “analyzing these cases to determine their status,” according to a letter IRS officials sent to Congress.

The cloudy status of some taxpayers who have potentially become Obamacare/ACA “mandate scofflaws” (in some cases) was originally the anticipated source and point of contention between the 27 states which filed to sue the federal government over the “Constitutionality” of “mandated” healthcare coverage. The number of states filing lawsuits also coincided with the states graphically depicted in the chart below (from Wikiepedia.org) which declined federal funding for creating “state-run insurance exchanges” (instead “defaulting” to the federally-run Healthcare.gov exchanges) and conversely refusing federal funding for expansions of Medicaid coverage for the poor-to-low-income Americans at the 138-percent and below Federal Poverty Line for coverage).

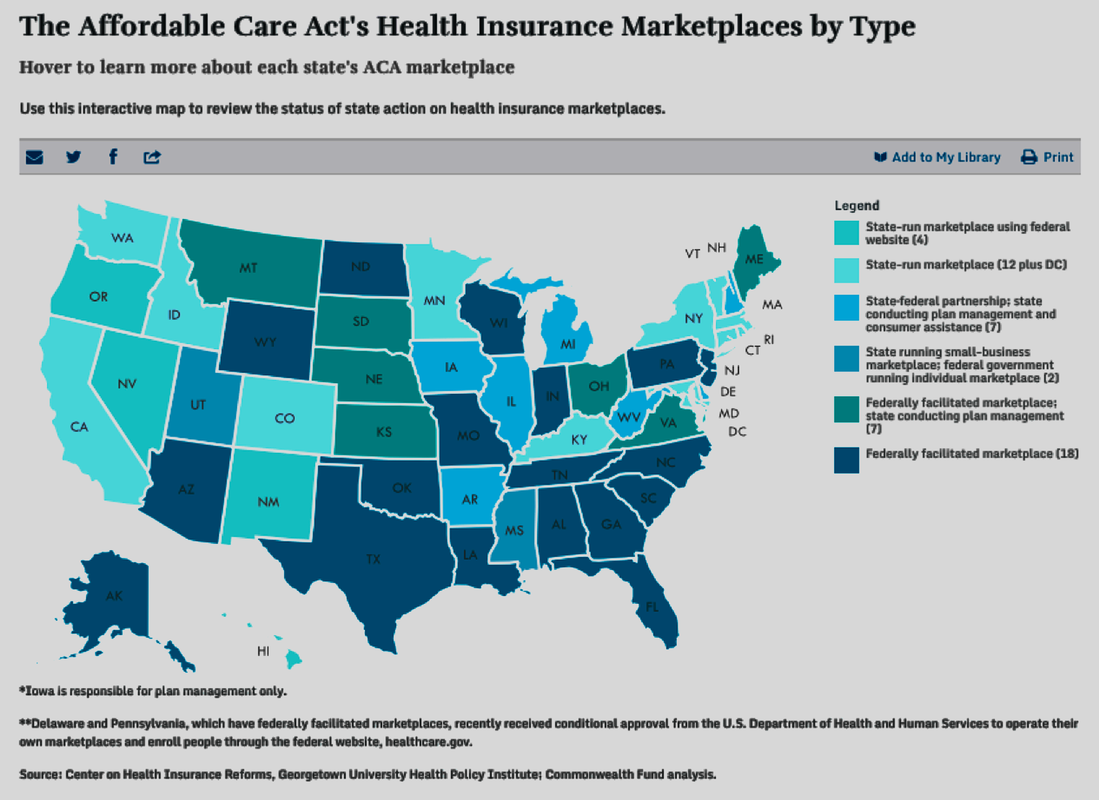

What America has is a hodge-podge mix of ACA/Obamacare’s brokered state- and federally-managed “public exchange” models: State-run insurance marketplace exchanges (12 states and the District of Columbia); state-run marketplaces using the (federal) Healthcare.gov website portal (4 states); state-federal partnerships, featuring the state running plan management and consumer assistance (7 states); and the bifurcated state-run small business marketplace and federal government-run individual marketplace in two states (as depicted in the top four lighter blue color-coded legend in the Commonwealth Fund-produced chart below).

Not surprisingly, all but two of the remaining 27 states — those who sued the federal government over the “Constitutionality” of mandated health insurance and marketplace exchanges — instead refused state funding and participation, but nonetheless “defaulted” to the “federally-facilitated” Healthcare.gov national marketplace exchange web portal for their residents to choose from available participating health insurance plans.

Not surprisingly, all but two of the remaining 27 states — those who sued the federal government over the “Constitutionality” of mandated health insurance and marketplace exchanges — instead refused state funding and participation, but nonetheless “defaulted” to the “federally-facilitated” Healthcare.gov national marketplace exchange web portal for their residents to choose from available participating health insurance plans.

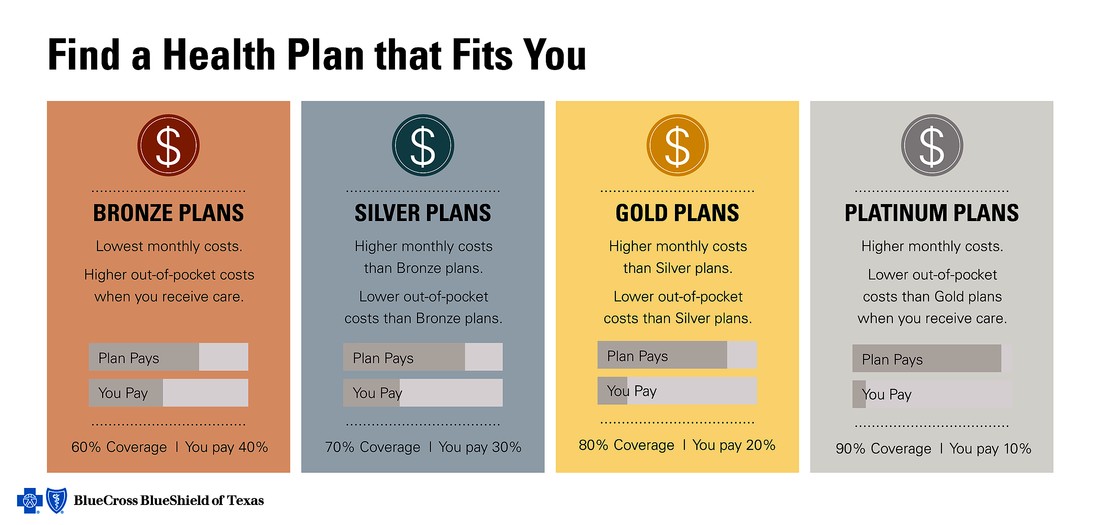

Under the framework of the state- and federal-run “health insurance marketplaces” (including the hybrid state-federal partnership exchanges) set forth in the Affordable Care Act, the Department of Health & Human Services crafted a four-tiered, “metallic” color-coded marketing structure based on the “actuarial level” of progressive health insurance coverage. As illustrated in the graphic depiction below (from nonprofit-based Blue Cross/Blue Shield of Texas’ website), the lowest-cost base premiums are “Bronze Plans,” which also represents the highest “out-of-pocket costs” to consumers who may consider themselves with lower health risks and/or not being able to afford as much in the “upfront” monthly premium charges.

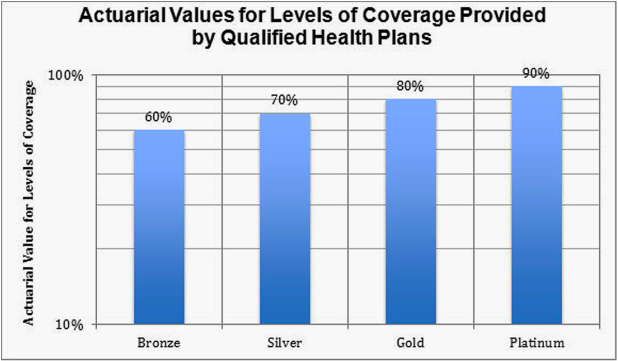

What you can ascertain from the above and below graphics is that the “actuarial levels” on what is financially “covered” by the health insurance carrier participating in the health insurance exchanges. As could be expected of the ACA’s guidelines on the tiered metallic plans, the lowest-cost Bronze Plan features a 60-percent actuarial level, leaving the exchange consumer to carry the burden of 40-percent of medical costs. The scale on actuarial coverage goes up in 10-percent increments for the Silver, Gold and Platinum plans from 70- to 90-pecent actuarial level coverage on the nationalized plan layout.

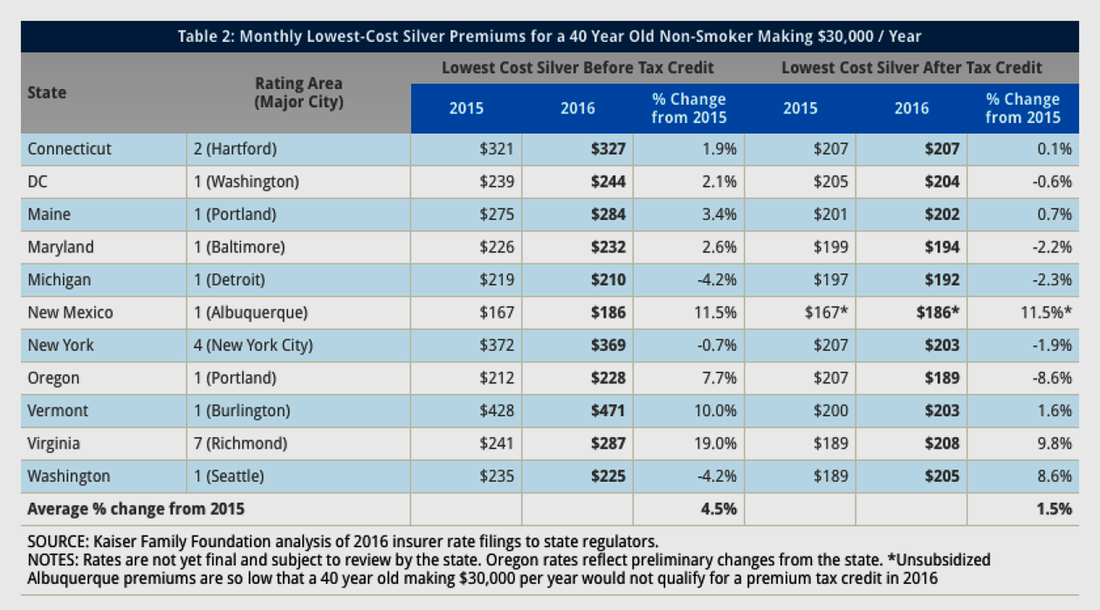

According to Kaiser Family Foundation, 68-percent of consumers in ACA state- and federally-run (and hybrid) exchanges opt for Silver Plan-level insurance premiums nationally. That’s why KFF chose to get a sampling of the “lowest cost” Silver-level plans in 10 select states’ largest city metropolitan areas and the District of Columbia (Washington) for a 40-year-old non-smoker making $30,000 per-year (seeking an “individual premium”) in the chart below to gauge typical pricing plan costs and whether there were annual decreases or increases from 2015 to 2016 plans.

Across the 11 major metro areas, Burlington, Vermont came in on the high end at $471 per-month costs before federal tax credit while Detroit, Michigan and Albuquerque, New Mexico came in at lowest range $210 per-month (subsidized) and $186 per-month (unsubsidized) in 2016, respectively — keeping in mind that 70-percent actuarial level means the individual consumer will pay the other 30-percent of medical costs (not counting other deductible and co-pay costs, too).

What’s most interesting is that 11 exchanges offered consumers premiums at an average $278 per-month charge for the “lowest cost” Silver plan before tax), a rise of 4.5-percent over the comparable 2015 average. After-tax credits from the federal government (based on several factors including income at 100- to 400-percent Federal Poverty Levels and the metallic level of insurance coverage), however, the “after tax credits” offer a roughly 28-percent credit to taxpayers, translating to a comparable $199 per-month premium average across the 11 exchanges and a smaller, adjusted 1.5-percent increase over 2015 for the comparable individual silver plan premium.

Across the 11 major metro areas, Burlington, Vermont came in on the high end at $471 per-month costs before federal tax credit while Detroit, Michigan and Albuquerque, New Mexico came in at lowest range $210 per-month (subsidized) and $186 per-month (unsubsidized) in 2016, respectively — keeping in mind that 70-percent actuarial level means the individual consumer will pay the other 30-percent of medical costs (not counting other deductible and co-pay costs, too).

What’s most interesting is that 11 exchanges offered consumers premiums at an average $278 per-month charge for the “lowest cost” Silver plan before tax), a rise of 4.5-percent over the comparable 2015 average. After-tax credits from the federal government (based on several factors including income at 100- to 400-percent Federal Poverty Levels and the metallic level of insurance coverage), however, the “after tax credits” offer a roughly 28-percent credit to taxpayers, translating to a comparable $199 per-month premium average across the 11 exchanges and a smaller, adjusted 1.5-percent increase over 2015 for the comparable individual silver plan premium.

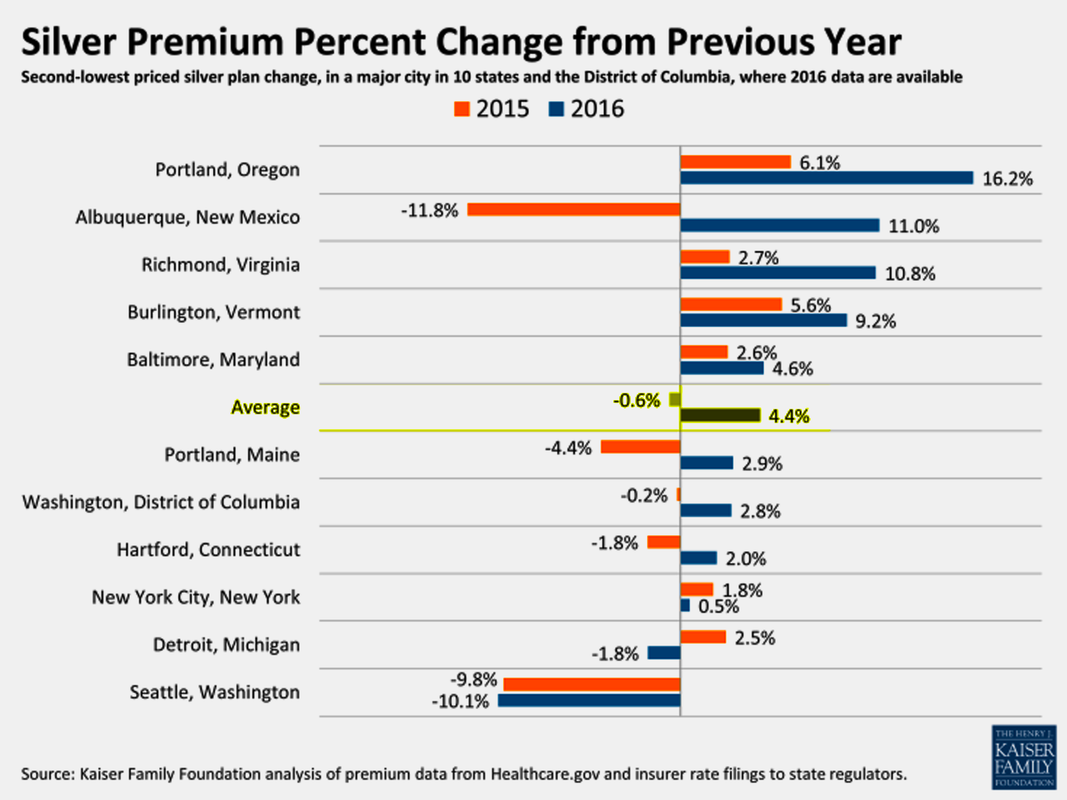

In another research brief Kaiser Family Foundation studying pricing for “second lower silver plan premium costs” across the same 11 major cites found some widely varying pricing increases emerging in 2016. Coming off a major 11.8-percent average pricing decrease, Albuquerque, New Mexico, nonetheless erased that with an 11.0-percent increase in 2016. Outside of Seattle, Washington registering welcome 9.8-percent and 10.1-percent decreases in pricing in 2015-16, 9 of the other 11 major cities registered pricing increases in 2016. Among the 11 cities KFF researched, there was a 0.6-percent decrease in premiums for the inaugural 2014 year of the insurance exchange marketplaces, but 2016 has marked a return to escalating premiums at an average 4.4-percent pricing increase for 2016.

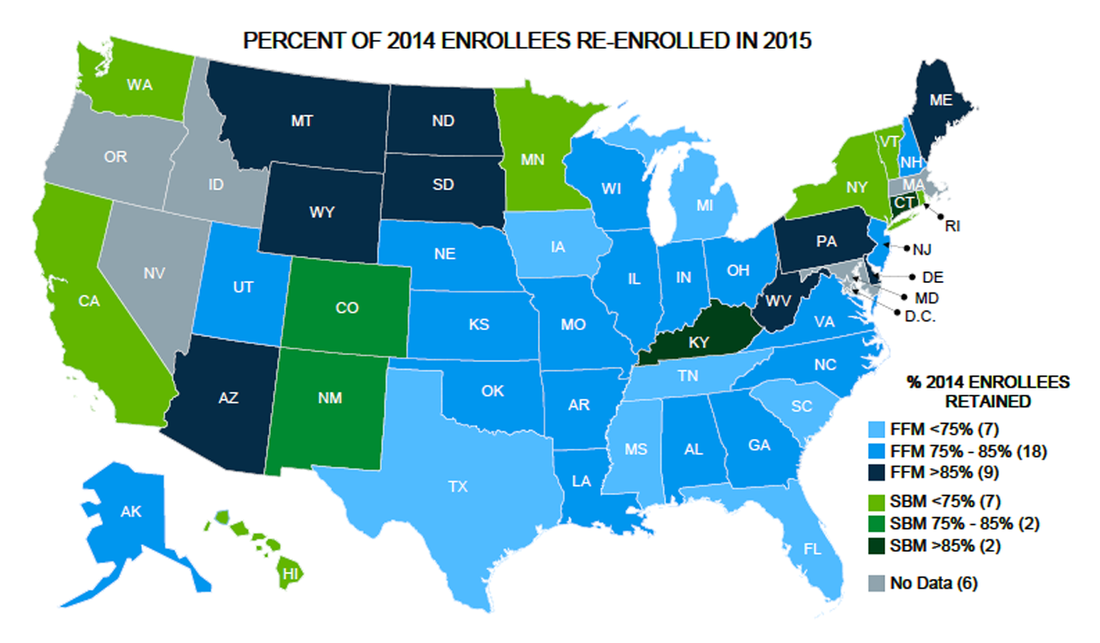

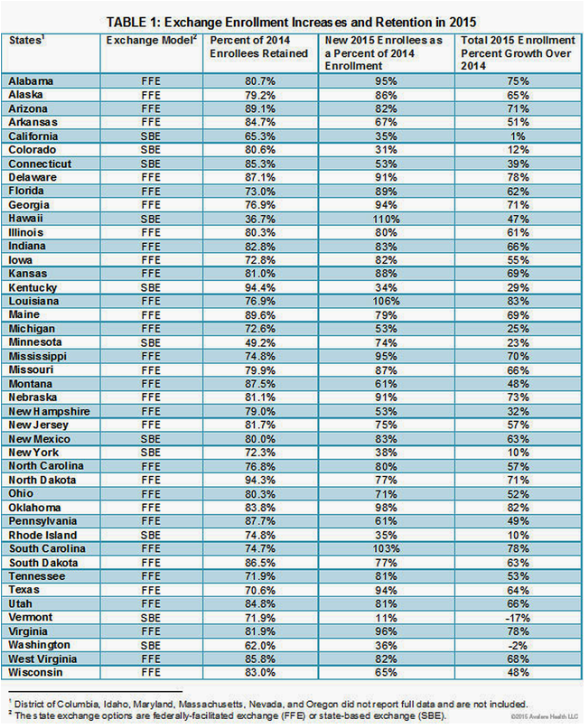

Since the launch of the ACA/Obamacare state-based (SBE) and federally-facilitated (FFE) public insurance exchanges starting in early 2014, there has been some success – albeit muted by mixed returns from the higher population states – in the retention of enrollees for its second year (2015) has been flirting between in the 75- to 85-percent range in a 27 of the 34 “default” Federally-Facilitated Exchanges, according to pair of charts (below) from Alavere Health research. Ironically, in the State-Based Exchanges originally envisioned by the ACA as the “model” exchange structure qualifying for federal funding, seven of the 11 “reporting” exchanges cited retention rates below 75-percent year-to-year.

Among the most successful of SBE marketplaces is Kentucky’s Kynect insurance portal, which retained just over 94-percent of its enrollees and grew its 2015 enrollment by 29-percent. Connecticut, another of the lower-population SBE insurance exchanges, scored 85.3-percent retention from is year-one enrollment and 2015 enrollment by 39-percent from the year-ago period. Among the federally-facilitated exchanges, such traditionally Republican-led states (most of which participated in the lawsuits against the federal government regarding “mandated” insurance) as North Dakota (94.4-percent retention of 2014 enrollees), Maine (89.6%), Arizona (89.1), Pennsylvania (87.7%), Delaware (87.1%), South Dakota (86.5%), West Virginia (85.8%), Utah (84.8%), Arkansas (84.7%), and Oklahoma (83.8%) recorded the best retention and year-to-year growth rates.

In the larger populations states like California, running Covered California as a SBE marketplace exchange, its first-year retention was 65.3-percent and second-year growth was just 1-percent for 2015. New York, also running an SBE, had just 72.3-percent retention and 10-percent growth. The two most populous states in the union most likely suffered the greater customer churn because consumers conversely have larger “private-market” health insurance and community health plan competition and choices by a relative margin over the lower population states.

In the larger populations states like California, running Covered California as a SBE marketplace exchange, its first-year retention was 65.3-percent and second-year growth was just 1-percent for 2015. New York, also running an SBE, had just 72.3-percent retention and 10-percent growth. The two most populous states in the union most likely suffered the greater customer churn because consumers conversely have larger “private-market” health insurance and community health plan competition and choices by a relative margin over the lower population states.

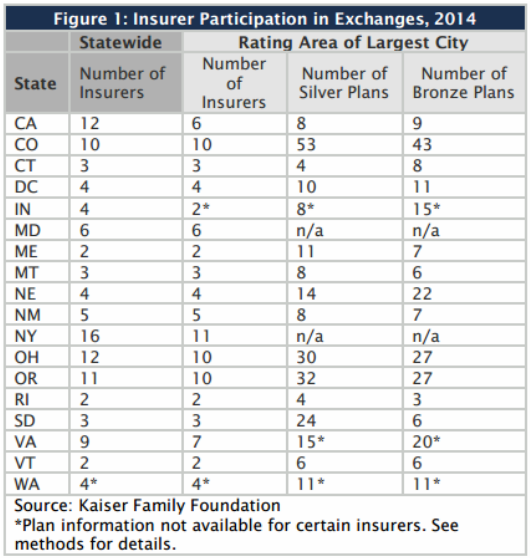

Nevertheless, the retention figures are expected to go lower for 2016 and 2017 as the number of participating health insurers decline in both the State-Based Exchanges and Federally-Facilitated Exchanges. According to the Kaiser Family Foundation table below, consumers in states like California, Colorado, New York, Ohio, and Oregon are anomalies in terms of larger number of participating insurers and the number of Bronze and Silver-tier lower-cost plans available in their largest cities and counties.

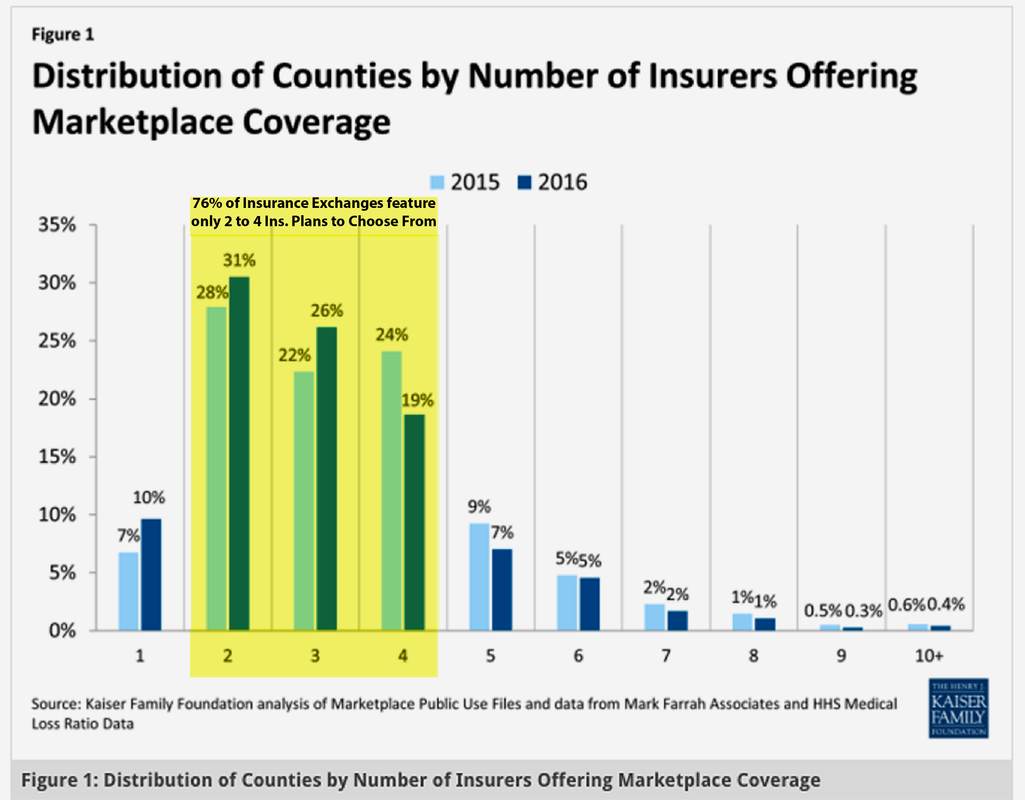

In fact, the number of participating health insurance carriers is decreasing to alarmingly low numbers in 2015 and 2016, according to KFF research data below. The paucity of choice and competitively priced plans in the ACA/Obamacare-inspired “mandated marketplaces” is reflected by the fact that 76-percent of state exchanges feature only two to four participating insurance carriers. This trend is also a consequence of the long-standing “consolidation” and “monopolization” of state market shares controlled by the handful of antitrust-exempt For-Profit/Big Health Insurance carriers.

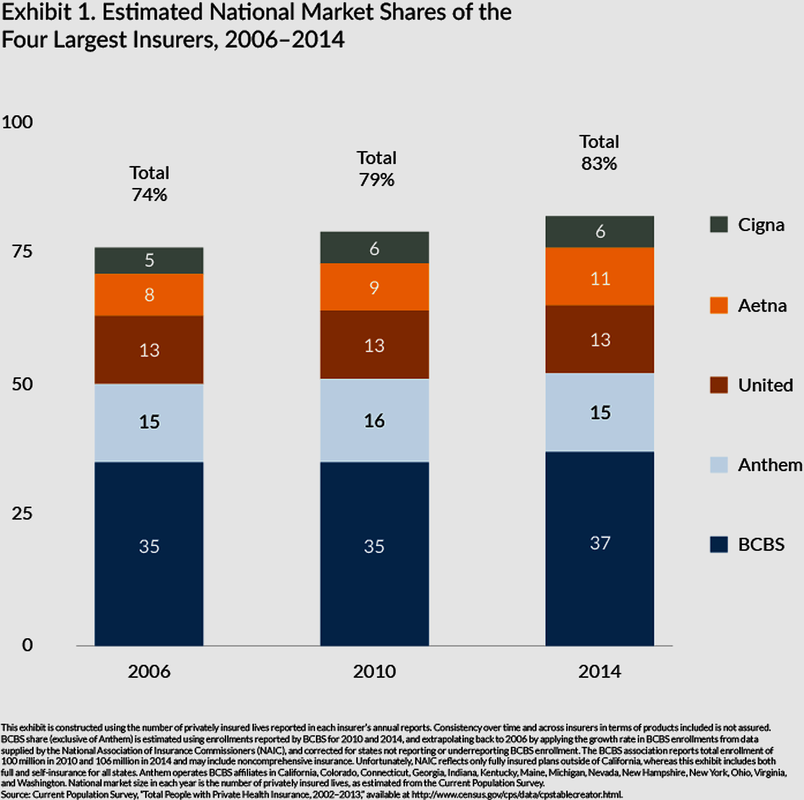

That market share concentration among “The Top Five Health Insurance Carriers” has been only getting WORSE over the last ten years. In this KFF bar chart below, it is inescapable that the antitrust-exempt monopolists of Big Health Insurance — Cigna, Aetna, UnitedHealth Group, Anthem and Blue Cross/Blue Shield licensees (either for-profit or nonprofit operators) — have seen their “estimated national [total] market shares” increase from 74-percent in 2006 to over 83-percent in 2014.

What places the future of the ACA/Obamacare marketplace in serious question is how UnitedHealthcare recently announced that it is going to initially “pull out” of 17 of the 34 state- and federally-run exchanges by the start of 2017 (a list of 16 of the “confirmed” states is listed below). UnitedHealth claims that by participating in the exchanges – where it serves about 800,000 policy-holders (or a 6 percent market share in the ACA marketplaces – it had too many higher risk patients to carry while also bearing the lower-cost plans to put it in a “money losing” situation. Still, UnitedHealth reported $157 BILLION in gross revenue and just over $5 BILLION in net income in fiscal year 2015 (ending Dec. 31, 2015) despite participating in the ACA-created exchanges since 2014.

Like UnitedHealth, another For-Profit/Big Health Insurer Humana — currently in the midst of a proposed merger in a takeover by Aetna awaiting final federal regulatory approval — has stated plans to conduct “product exits” in most, if not all, of ACA marketplaces by 2017. For the first quarter ending March 31, 2016, Humana reported it had incurred a nearly 46-percent year-to-year quarterly drop in earnings, with $13.8 BILLION in revenue and net income of $234 million. Humana officials cited declining revenue returns stemming from a 21-percent in plan enrollees (or 232,200 premium holders) to 875,000 members from the ACA public exchanges in the most recent quarter (down from 1.1 million customers in the year-ago quarter).

Nevertheless, some Wall Street analysts have pegged some of Humana’s losses due “costs” associated with the ongoing Aetna merger process. However, Aetna has claimed to fare somewhat better financially in the ACA public exchanges and, in potentially absorbing what might be left of Humana’s exchange business, is said to be considering expanding its participation in some key state exchanges. Another For-Profit/Big Health Insurance carrier, Centene, completed a takeover of former competitor Health Net, which increases its presence in the ACA public exchanges and having it consider further expansion into other state marketplaces.

Anthem, a publicly-traded owner/operator of “for-profit-based” Blue Cross/Blue Shield franchises in 14 states, is also talking about some ACA public exchange plan expansions. Given that a handful of Big Health Insurance carriers hold a dominant 83-percent market share of the overall U.S. insurance marketplace, don’t expect any new choices and increased competition anytime soon.

Nevertheless, some Wall Street analysts have pegged some of Humana’s losses due “costs” associated with the ongoing Aetna merger process. However, Aetna has claimed to fare somewhat better financially in the ACA public exchanges and, in potentially absorbing what might be left of Humana’s exchange business, is said to be considering expanding its participation in some key state exchanges. Another For-Profit/Big Health Insurance carrier, Centene, completed a takeover of former competitor Health Net, which increases its presence in the ACA public exchanges and having it consider further expansion into other state marketplaces.

Anthem, a publicly-traded owner/operator of “for-profit-based” Blue Cross/Blue Shield franchises in 14 states, is also talking about some ACA public exchange plan expansions. Given that a handful of Big Health Insurance carriers hold a dominant 83-percent market share of the overall U.S. insurance marketplace, don’t expect any new choices and increased competition anytime soon.

In fact, with a Republican majority in both houses of Congress voting for repeal of the Affordable Care Act unsuccessfully over 60 times and filing scores of lawsuits over its Constitutionality since 2010, conservatives most recently got U.S. District Judge Rosemary Collyer (an appointee from President George W. Bush’s administration) to rule that the Obama administration cannot spend billions of dollars in federal funds to provide subsidies under the law known as Obamacare to private insurers without the approval of Congress. At issue in the case, brought by the Republican-led House of Representatives, are reimbursements to insurance companies to compensate them for reductions that the law requires them to make to customers' out-of-pocket medical payments.

The ruling will not have an immediate effect on the law because the judge put the decision on hold pending an expected appeal by the Obama administration. But it adds to uncertainty over the future of President Obama's signature domestic policy achievement ahead of the November 8, 2016 presidential and congressional elections, including whether enough health insurers will continue to participate in the ACA public exchanges.

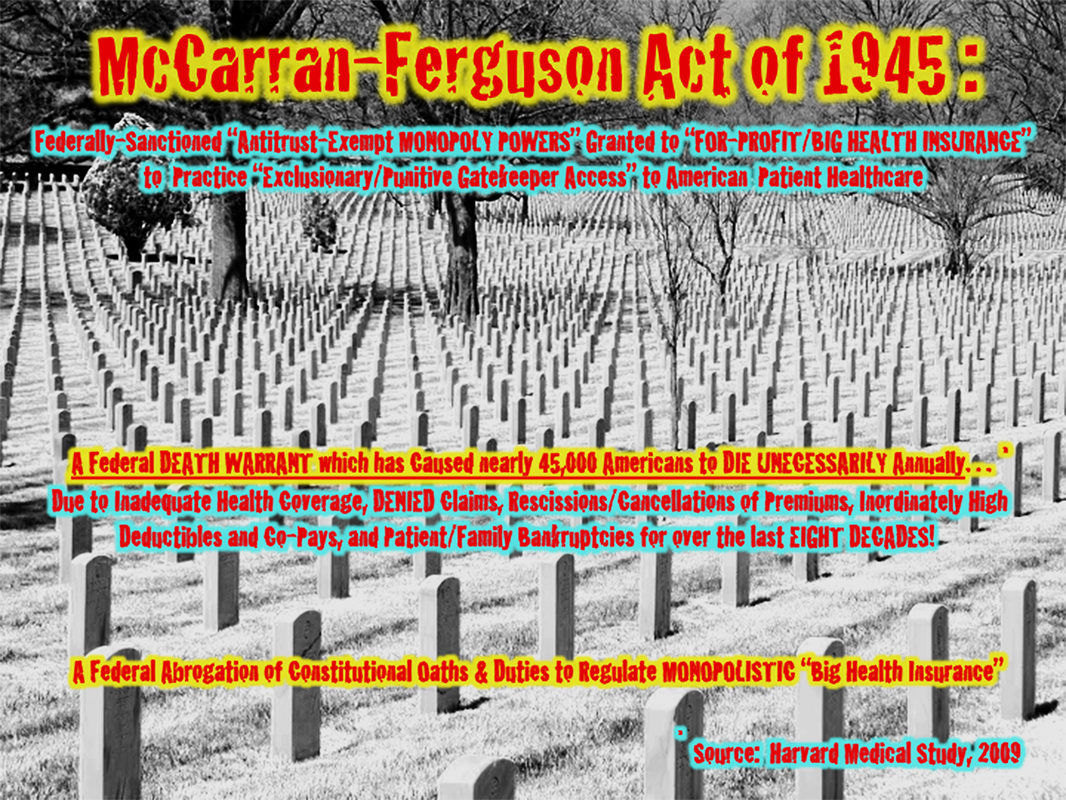

The long-standing, entrenched nature of antitrust-exempt, monopoly-based “For-Profit/Big Health Insurance has also pretty much made it FREE of any federal regulation and oversight for the last THREE-QUARTERS of a century. That’s due in large part to Congress passing one of the most “unconstitutional” pieces of federal legislation, the McCarran-Ferguson Act of 1945, which essentially gives the Big Health Insurance Carriers an “exemption” from being regulated by the federal government (the feds leave it up to largely toothless “state insurance commissions” typically chaired and stocked with former For-Profit/Big Insurance executives to "regulate" them).

The ruling will not have an immediate effect on the law because the judge put the decision on hold pending an expected appeal by the Obama administration. But it adds to uncertainty over the future of President Obama's signature domestic policy achievement ahead of the November 8, 2016 presidential and congressional elections, including whether enough health insurers will continue to participate in the ACA public exchanges.

The long-standing, entrenched nature of antitrust-exempt, monopoly-based “For-Profit/Big Health Insurance has also pretty much made it FREE of any federal regulation and oversight for the last THREE-QUARTERS of a century. That’s due in large part to Congress passing one of the most “unconstitutional” pieces of federal legislation, the McCarran-Ferguson Act of 1945, which essentially gives the Big Health Insurance Carriers an “exemption” from being regulated by the federal government (the feds leave it up to largely toothless “state insurance commissions” typically chaired and stocked with former For-Profit/Big Insurance executives to "regulate" them).

For just over seven decades under McCarran-Ferguson Act, the federal government essentially turned blind eyes to the systemic marketplace abuses of consumer-patients who fell victim to rampant, long-standing pattern of DENIED claims (especially in regards to what For-Profit/Big Health Insurers regularly cited as “experimental medical procedures”), rescissions/cancellations of premiums because certain targeted “chronically ill patients” had fallen into certain “higher risk ratio pools,” and other forms of exclusionary, punitive and rationing business practices. McCarran-Ferguson has essentially allowed For-Profit/Big Health Insurance monopolists to become the ultimate, middlemen “gatekeepers” on healthcare access in America’s patchwork marketplace for 71 years running.

During the height of the largely “closed-door” Healthcare Reform debates in the Senate and House, Sen. Patrick Leahy (D-Vermont) and Rep. John Conyers (D-Michigan) both introduced and authored (in their respective houses of Congress) concurrent bills calling for the “repeal” of the McCarran-Ferguson Act. To the relief of consumer advocates, the House had voted affirmatively for its repeal. However, during the midnight hours on the eve of the Affordable Care Act’s passage, then-Senate Majority Leader Sen. Harry Reid (D-Nevada) had quietly announced that Leahy’s senate repeal bill had been “tabled for a lack of a quorum,” essentially a coded message that the For-Profit/Big Healthcare Lobby had gotten to a majority of the senators to ignore that effort. In all four bills seeking to repeal McCarron-Ferguson had been introduced to the House and Senate over the last 10 years (including by Conyers again in January 2015) – all of them meeting the typical “wall of silence and indifference” from a Congress, which refuses to live up its Constitutional oath of “Serving in the Public Trust.”

The passage of the Patient Protection and Affordable Care Act of 2010, however, did offer a few symbolic attempts in the federal legislation, somewhat briefly including the end of rescissions of health insurance policies and DENIAL of claims because of relatively higher costs associated with urgent-care surgical and elective medical procedures (some falling into the “experimental” category).

Nevertheless, there have been some widespread accounts that the For-Profit/Big Health Insurance monopolists are up to their old tricks on “denials of claims,” including USA Today reporting on a 37-year-old man with life-threatening cystic fibrosis who has difficulty with breathing, but his doctors recommended a new life-saving “breakthrough drug” called Kalydeco, which costs $25,000 per-month for prescription treatments. As it turns it, the man’s insurance carrier, UnitedHealth Group approved the medication for his sister (diagnosed for the same mutation of cystic fibrosis, but the brother is denied four times because the drug is “not FDA approved” at the moment (July 2013) and a UnitedHealth claim reviewer says his condition is NOT life-threatening while his sister’s same medical condition is deemed life-threatening.

A close friend of mine who also works in the “diagnostic” area of a family clinic has repeatedly related to me stories about how her clinic’s “at-risk” patients have been routinely denied claims to have certain Electrocardiogram (EKG), Magnetic Resonance Imaging (MRI) and CAT Scan (CT) diagnostic tests completed -- even though the patients received a doctors’ “pre-authorization” or “referral” to do the diagnostic procedure. It may be a more common practice because your claim might be denied by the Health Insurance Carrier if the a “pre-authorization” is lacking a formal doctor’s statement, which my friend said is sometimes still ignored by the health insurance provider.

Out of the passage of the sausage-made Affordable Care Act, it was thought the Big Health Insurance monopolists made a big concession regarding the industry’s stand on pre-existing conditions. But the bill has a giant loophole: insurers can continue to cancel policies in cases of alleged “fraud or intentional misrepresentation” by premium holders as they do now, according to Huffington Post’s report dating back to May 25, 2011. “Readers have no doubt hear of or read about how low the permitted bar is now for insurers to rescind policies. And when are insurers most likely to look to find grounds not to pay for treatment? When you most need it, of course, when you have a serious, expensive ailment,” HuffPo’s article noted.

There also other published reports like one in August 2014 from the Las Vegas Journal Review about a woman who gave premature birth to a daughter who still needed two subsequent surgeries and a 40-day stay at Summerlin Hospital there. Unfortunately, their health insurer, Blue Cross Blue Shield of Nevada cancelled their policy retroactively after the hospital had a “typo” on one of the claims listing the mother’s birthday as one year earlier – with BCBS citing the intentional misrepresentation and fraud provision in getting out of the daughter’s surgeries and extended hospital stay.

The Huffington Post account in “An Inglorious End to the Promise of Reform” best summed up the “Catch-22” nature of the ACA’s “individual mandate” on obtaining healthcare in America: “Individual mandate was the top priority of the insurance industry, which also succeeded in fending off meaningful restraints of its predatory pricing practices. The likely outcome is that far too many people will still face health care insecurity or medical bankruptcy due to ever rising out-of-pocket costs, or continue to skip needed medical care because of the high prices. Indeed, discouraging provision of care as the preferred way to control costs, rather than rein in the pricing practices of the insurance and drug giants, is a central tenet of the insurance industry and conservative policy wonk.”

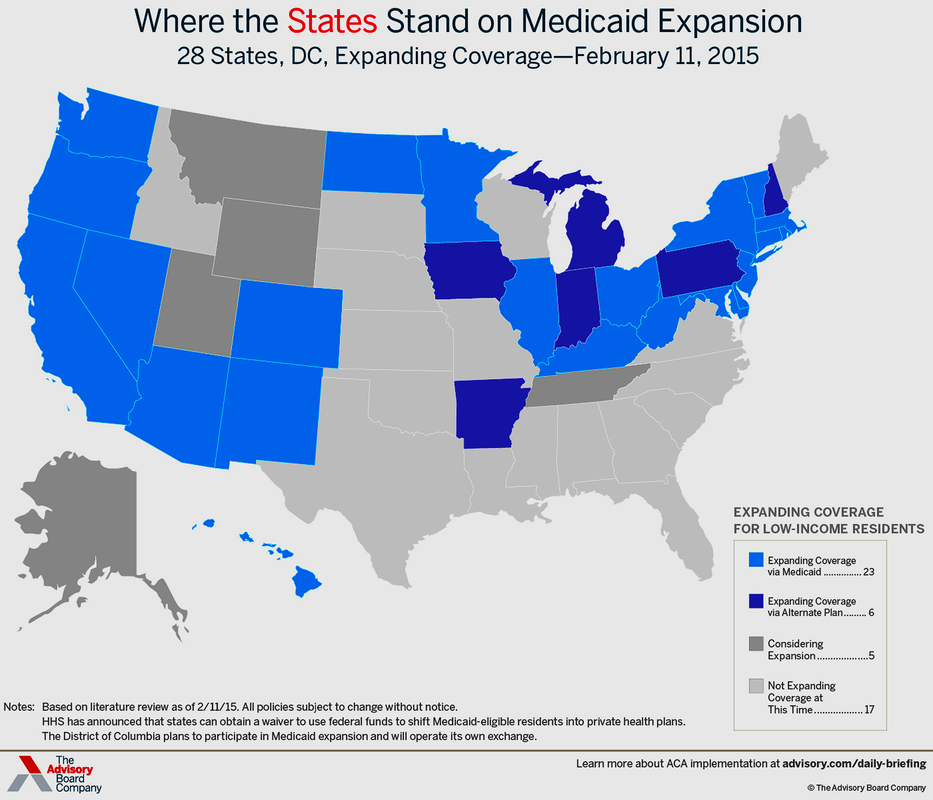

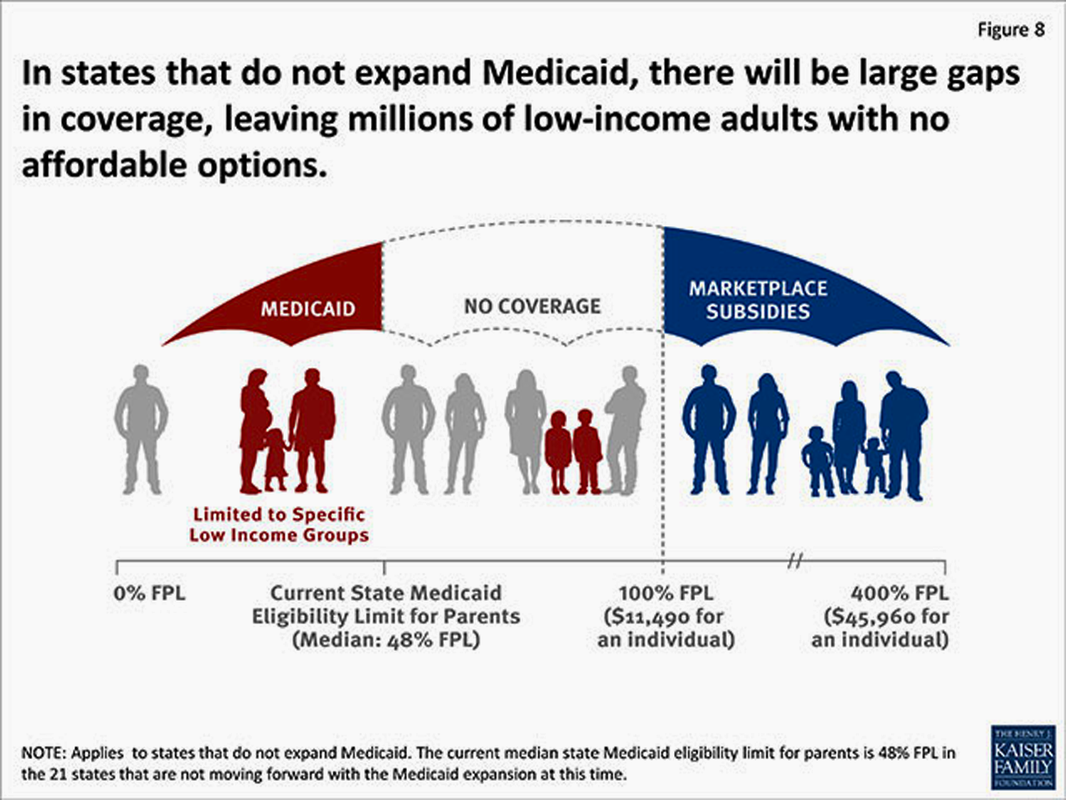

In fact, largely coinciding with how Republican-led “Red States” had already refused to join the ACA/Obamacare public exchanges with “state funding and operational participation,” these are mainly the states also refusing to expand Medicaid plan offerings (even though it is federally funded) to lower-income to indigent individuals and families falling within 138-percent of the Federal Poverty Line. As the Advisory Board Company map below illustrates, 22 of the mostly Southern and Plains states declining to participate in the Medicaid Expansion, five of the darker gray-colored states are “considering expansion,” but 17 of the lighter gray states are “not expanding coverage” at this time (dating back to February 11, 2015).

During the height of the largely “closed-door” Healthcare Reform debates in the Senate and House, Sen. Patrick Leahy (D-Vermont) and Rep. John Conyers (D-Michigan) both introduced and authored (in their respective houses of Congress) concurrent bills calling for the “repeal” of the McCarran-Ferguson Act. To the relief of consumer advocates, the House had voted affirmatively for its repeal. However, during the midnight hours on the eve of the Affordable Care Act’s passage, then-Senate Majority Leader Sen. Harry Reid (D-Nevada) had quietly announced that Leahy’s senate repeal bill had been “tabled for a lack of a quorum,” essentially a coded message that the For-Profit/Big Healthcare Lobby had gotten to a majority of the senators to ignore that effort. In all four bills seeking to repeal McCarron-Ferguson had been introduced to the House and Senate over the last 10 years (including by Conyers again in January 2015) – all of them meeting the typical “wall of silence and indifference” from a Congress, which refuses to live up its Constitutional oath of “Serving in the Public Trust.”

The passage of the Patient Protection and Affordable Care Act of 2010, however, did offer a few symbolic attempts in the federal legislation, somewhat briefly including the end of rescissions of health insurance policies and DENIAL of claims because of relatively higher costs associated with urgent-care surgical and elective medical procedures (some falling into the “experimental” category).

Nevertheless, there have been some widespread accounts that the For-Profit/Big Health Insurance monopolists are up to their old tricks on “denials of claims,” including USA Today reporting on a 37-year-old man with life-threatening cystic fibrosis who has difficulty with breathing, but his doctors recommended a new life-saving “breakthrough drug” called Kalydeco, which costs $25,000 per-month for prescription treatments. As it turns it, the man’s insurance carrier, UnitedHealth Group approved the medication for his sister (diagnosed for the same mutation of cystic fibrosis, but the brother is denied four times because the drug is “not FDA approved” at the moment (July 2013) and a UnitedHealth claim reviewer says his condition is NOT life-threatening while his sister’s same medical condition is deemed life-threatening.

A close friend of mine who also works in the “diagnostic” area of a family clinic has repeatedly related to me stories about how her clinic’s “at-risk” patients have been routinely denied claims to have certain Electrocardiogram (EKG), Magnetic Resonance Imaging (MRI) and CAT Scan (CT) diagnostic tests completed -- even though the patients received a doctors’ “pre-authorization” or “referral” to do the diagnostic procedure. It may be a more common practice because your claim might be denied by the Health Insurance Carrier if the a “pre-authorization” is lacking a formal doctor’s statement, which my friend said is sometimes still ignored by the health insurance provider.

Out of the passage of the sausage-made Affordable Care Act, it was thought the Big Health Insurance monopolists made a big concession regarding the industry’s stand on pre-existing conditions. But the bill has a giant loophole: insurers can continue to cancel policies in cases of alleged “fraud or intentional misrepresentation” by premium holders as they do now, according to Huffington Post’s report dating back to May 25, 2011. “Readers have no doubt hear of or read about how low the permitted bar is now for insurers to rescind policies. And when are insurers most likely to look to find grounds not to pay for treatment? When you most need it, of course, when you have a serious, expensive ailment,” HuffPo’s article noted.

There also other published reports like one in August 2014 from the Las Vegas Journal Review about a woman who gave premature birth to a daughter who still needed two subsequent surgeries and a 40-day stay at Summerlin Hospital there. Unfortunately, their health insurer, Blue Cross Blue Shield of Nevada cancelled their policy retroactively after the hospital had a “typo” on one of the claims listing the mother’s birthday as one year earlier – with BCBS citing the intentional misrepresentation and fraud provision in getting out of the daughter’s surgeries and extended hospital stay.

The Huffington Post account in “An Inglorious End to the Promise of Reform” best summed up the “Catch-22” nature of the ACA’s “individual mandate” on obtaining healthcare in America: “Individual mandate was the top priority of the insurance industry, which also succeeded in fending off meaningful restraints of its predatory pricing practices. The likely outcome is that far too many people will still face health care insecurity or medical bankruptcy due to ever rising out-of-pocket costs, or continue to skip needed medical care because of the high prices. Indeed, discouraging provision of care as the preferred way to control costs, rather than rein in the pricing practices of the insurance and drug giants, is a central tenet of the insurance industry and conservative policy wonk.”

In fact, largely coinciding with how Republican-led “Red States” had already refused to join the ACA/Obamacare public exchanges with “state funding and operational participation,” these are mainly the states also refusing to expand Medicaid plan offerings (even though it is federally funded) to lower-income to indigent individuals and families falling within 138-percent of the Federal Poverty Line. As the Advisory Board Company map below illustrates, 22 of the mostly Southern and Plains states declining to participate in the Medicaid Expansion, five of the darker gray-colored states are “considering expansion,” but 17 of the lighter gray states are “not expanding coverage” at this time (dating back to February 11, 2015).

Although the Healthcare.gov map illustration below dates back to April 2014, the graphic provides a fair representation of how many Americans will remain “uninsured” due to a lack of free, mostly federally-subsidized Medicaid health plan coverage in those holdout states. The Department of Health and Human Services and Centers of Medicare and Medicaid Services (CMS) estimated that a total of 5.7 million Americans would remain “uninsured” in the non-participating states. The two largest states with uninsured are Texas (1.2 million of its residents) and Florida (845,000) – both states do NOT collect state income taxes and offer less in terms of public “safety net” programs.

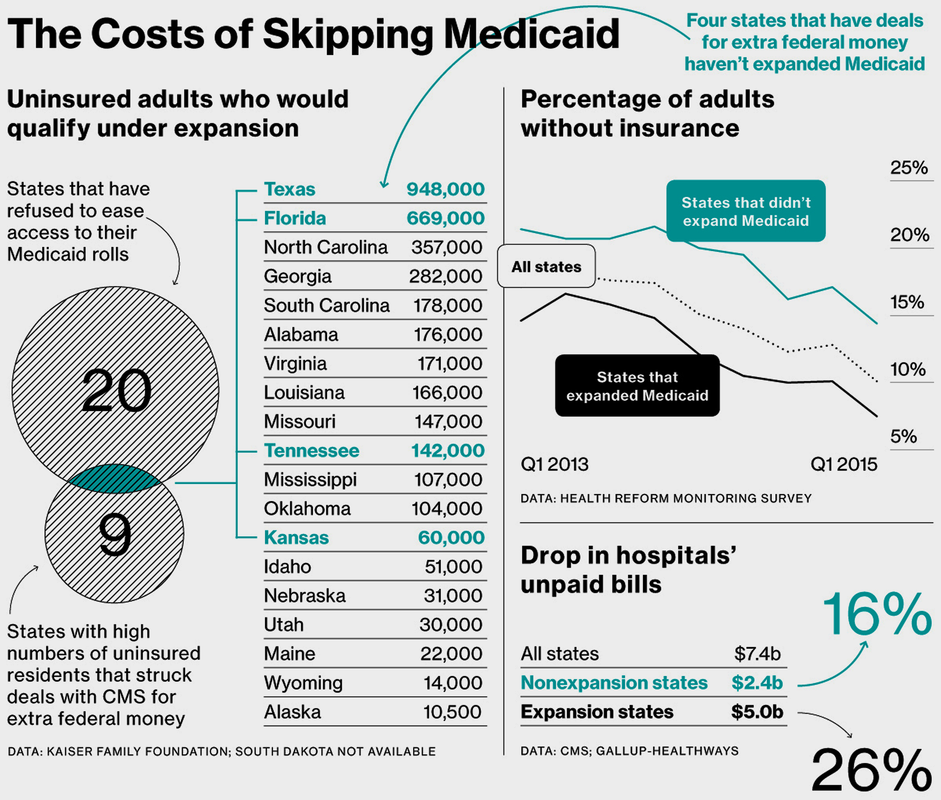

The biggest incentive is ACA’s promise of federal funds to cover the whole cost of newly qualified Medicaid patients for three years, until 2016, and at least 90 percent of the costs thereafter. However, by mid-2015 (as illustrated in the Bloomberg News-produced graphic below), there were still 20 states that refused to ease access to their Medicaid rolls. A few have been able to eat their cake and have it, too: Because of special arrangements that predate Obamacare, four states (Texas, Florida, Tennessee and Kansas) that haven’t expanded Medicaid have been getting billions each year in extra funding to pay for the care of people who are uninsured.

Florida and Texas are among nine states with high numbers of uninsured residents that struck deals with CMS for extra federal money to help hospitals, which are legally bound to provide care whether or not patients can pay. The arrangements, known as “uncompensated care pools,” are subject to periodic renewal and were also granted to Arizona, California, Hawaii, Kansas, Massachusetts, New Mexico, and Tennessee. Of those, only Kansas and Tennessee have joined Florida and Texas in continuing to resist Medicaid expansion.

Florida is the first to come up for review since the Affordable Care Act went into force. Florida Governor Rick Scott, a Tea Party conservative, opposed expanding Medicaid when he took office in 2011, then reversed himself in 2013, saying in a news conference that with Washington picking up the tab, “I cannot, in good conscience, deny Floridians the needed access to health care.” With his state legislature dominated by conservative Republicans, he wavered.

The “grandfathered” federal funding from CMS has allowed the four holdout states – Texas, Florida, Tennessee and Kansas – to reduce the number of uninsured residents of their states and similarly benefit, along with the “Medicaid expansion states,” to see that their states’ “uncompensated care pools” receive the federal funding to reduce hospital costs by $5 BILLION by the first quarter of 2015.

Florida and Texas are among nine states with high numbers of uninsured residents that struck deals with CMS for extra federal money to help hospitals, which are legally bound to provide care whether or not patients can pay. The arrangements, known as “uncompensated care pools,” are subject to periodic renewal and were also granted to Arizona, California, Hawaii, Kansas, Massachusetts, New Mexico, and Tennessee. Of those, only Kansas and Tennessee have joined Florida and Texas in continuing to resist Medicaid expansion.

Florida is the first to come up for review since the Affordable Care Act went into force. Florida Governor Rick Scott, a Tea Party conservative, opposed expanding Medicaid when he took office in 2011, then reversed himself in 2013, saying in a news conference that with Washington picking up the tab, “I cannot, in good conscience, deny Floridians the needed access to health care.” With his state legislature dominated by conservative Republicans, he wavered.

The “grandfathered” federal funding from CMS has allowed the four holdout states – Texas, Florida, Tennessee and Kansas – to reduce the number of uninsured residents of their states and similarly benefit, along with the “Medicaid expansion states,” to see that their states’ “uncompensated care pools” receive the federal funding to reduce hospital costs by $5 BILLION by the first quarter of 2015.

Nevertheless, with the number of uninsured Americans overall hovering at what is estimated at 20 million-plus citizens because of the state declining to participate in Medicaid expansion, the so-called “Medicaid Gap” is expected to widen again by 2017. Such a scenario is likely for federal funding taps closing if a victorious Republican presidential nominee (as its stands currently with Donald J. Trump being the presumptive nominee who might still face a “contested convention” this July in Cleveland) takes the White House and if the GOP retains majorities in both houses of Congress to finally succeed in legally repealing Obamacare.

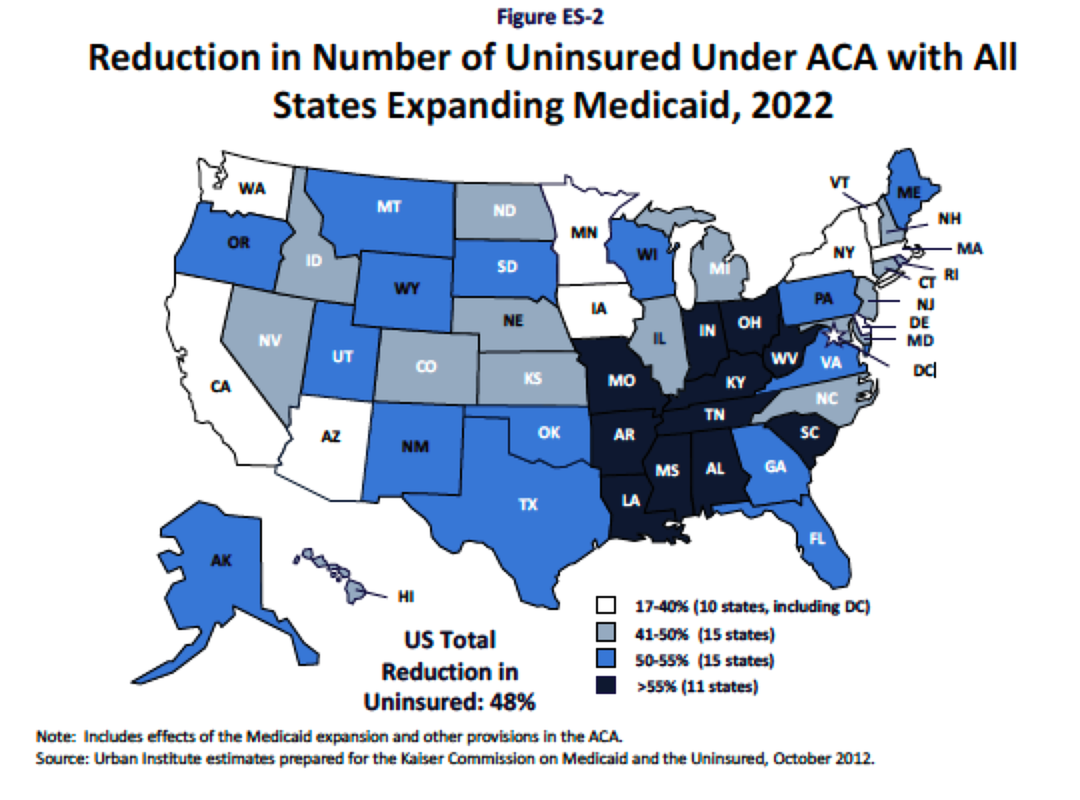

In May 2016, President Obama proudly announced that just under 13 million Americans gained healthcare coverage through the ACA-backed public insurance exchanges while another 7.5 million low-income/poor citizens qualified for Medicaid-sponsored health coverage in both the expansion and non-conforming, pre-Obamacare funded states. Urban Institute, in a research study commissioned by The Kaiser Commission on Medicaid and Uninsured (in the map below) answered a scenario that if “all states” participated in the expansion of Medicaid under the ACA bill by 2022, it projected that the level of uninsured Americans would translate to a 48-percent reduction overall – with the greatest 55 percent-plus reductions coming from the states currently refusing to partake in Medicaid expansion.

Despite the perceived “publicly-minded” efforts of the Obama administration and Democrats in Congress, which passed the Affordable Care Act by the narrowest of partisan margins in 2010, the number of Americans “falling outside the boundaries” of health coverage remains considerable. The “dilemma of the uncovered” – either unable to afford and ignoring the “mandated coverage penalties,” declining the ACA state-based or federally-facilitated public insurance exchanges and not qualifying or a resident in a noncompliant state for subsidized Medicaid health coverage – points to the overall number uninsured Americans floating at around a 10 percent-plus range at just over 22 MILLION or more citizens still lacking healthcare coverage in this country.

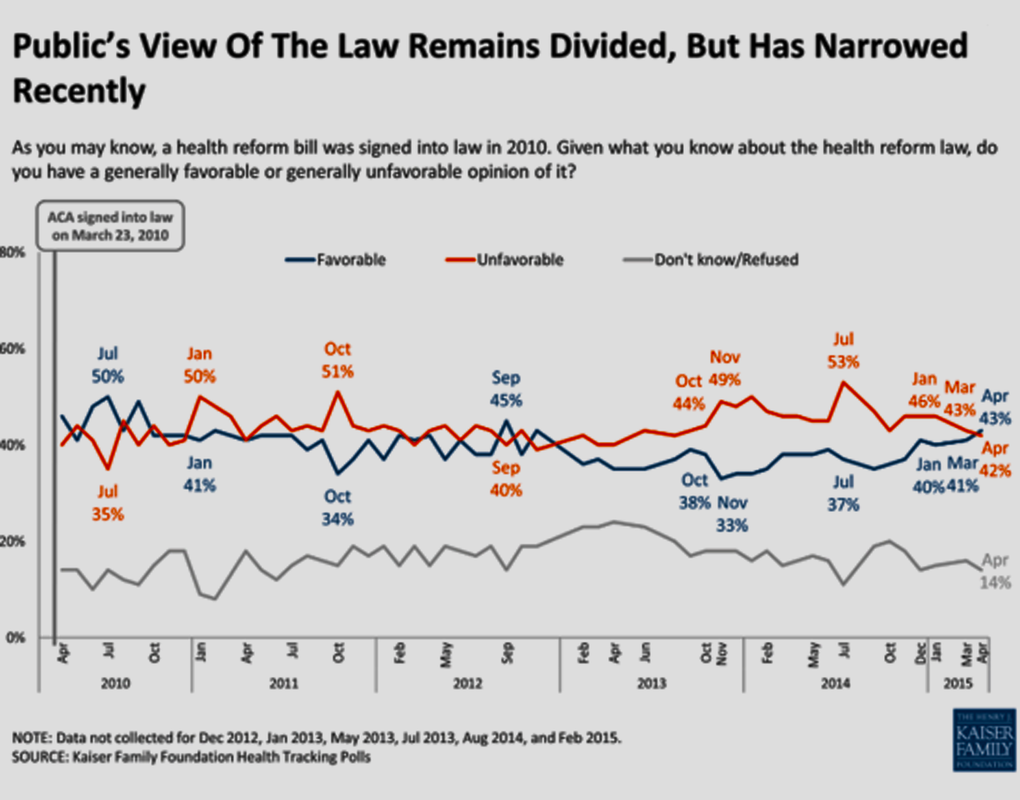

The American public remains the most telling barometer on Obamacare’s success and long-term viability, though. Like the states remaining divided on accepting or fighting “mandated” health coverage, the American public, according to Kaiser Family Foundation Health Tracking Polls (in the five-year poll of 2010-2015 attached below), remain almost evenly divided, but the trend line for Americans viewing Obamacare “favorably” rose from 37-percent in July 2014 to 43-percent in April 2015.

The American public remains the most telling barometer on Obamacare’s success and long-term viability, though. Like the states remaining divided on accepting or fighting “mandated” health coverage, the American public, according to Kaiser Family Foundation Health Tracking Polls (in the five-year poll of 2010-2015 attached below), remain almost evenly divided, but the trend line for Americans viewing Obamacare “favorably” rose from 37-percent in July 2014 to 43-percent in April 2015.

Most notably, the split in American public opinion on Obamacare is, perhaps, emblematic of the teetering nature of its potential to lose continued federal funding, especially if Republicans grab the White House and continue to hold majorities in both houses of Congress by January 2017. Outside of the great “external threats” politically for the Affordable Care Act facing a “successful” repeal vote in Congress, the inherent, ever-escalating “price-gouging increases” successfully engineered by the antitrust-exempt “For-Profit/Big Health Insurance” monopolists challenges the basic financial underpinnings of the ACA public insurance exchanges as well as the open “commercial marketplace” for both individual and family premium consumers.

Lastly, the number of states (20 or more) continuing to refuse to participate on state-level contributions to the expansion of Medicaid to provide subsidized health coverage for low-income/indigent Americans by suing the federal government over the Constitutionality of “mandated” health insurance coverage, is creating an ever-widening Grand Canyon-sized chasm for the ACA-participating states and federal government to continue “bridging.” It is still an inescapable fact that approximately 22 million Americans remain “uninsured” and “uncovered” when it comes to either needing urgent care treatment for a catastrophic illness or accident – leaving them in dire fear of ever facing such an event.

For the Americans who can either afford costly, artificially-inflated health coverage (remember the KFF research listed above, citing a 200 percent-plus increase in insurance premium costs from 1999 to 2015!) from the For-Profit/Big Health Insurance or qualify for tax credits and subsidies to buy slightly lower-cost plan coverage through the ACA public exchanges, they are still faced with ever-increasing, burden-shifting higher out-of-pocket DEDUCTIBLES and Co-Pay expenses laden onto their shoulders. Even the specter of facing “tax penalties” for NOT being in compliance with ‘mandated” health insurance coverage pales in comparison with the overriding fear of personal bankruptcy due to overwhelming, partially or fully “uncovered” medical costs that weighs heavily on most Americans’ psyches…every day of their lives.

Back in March 2010, nearing the final House and Senate congressional votes for the Affordable Care Act’s extremely narrow, partisan passage, one of the lone Democratic holdouts, then-Rep. Dennis Kuccinich (D-Ohio), was famously quoted during his long holdout, suggesting Obamacare’s blueprint was akin to “building a foundation on quicksand.” (Kuccinich had been a long-time advocate of a broader “Single-Payer Universal Healthcare” system.)

Well, the house is still standing, but all of the economic and political indicators suggest that the ACA/Obamacare’s current foundation is showing some cracks/fissures and badly in need of massive repairs or a Herculean-type overhaul if it is going to survive well into the next presidency and session of Congress starting in January 2017. #

– Michael A. Freeman

RSS Feed

RSS Feed